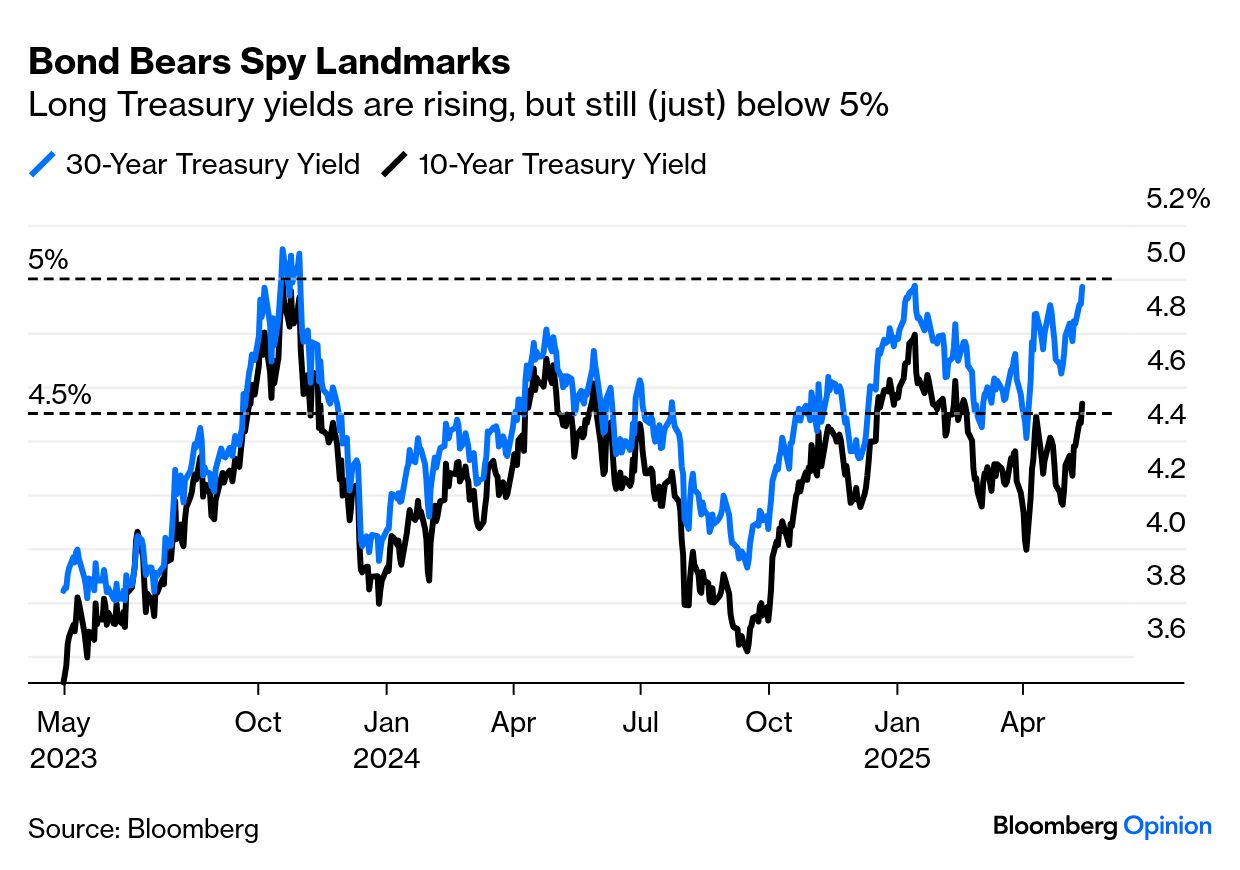

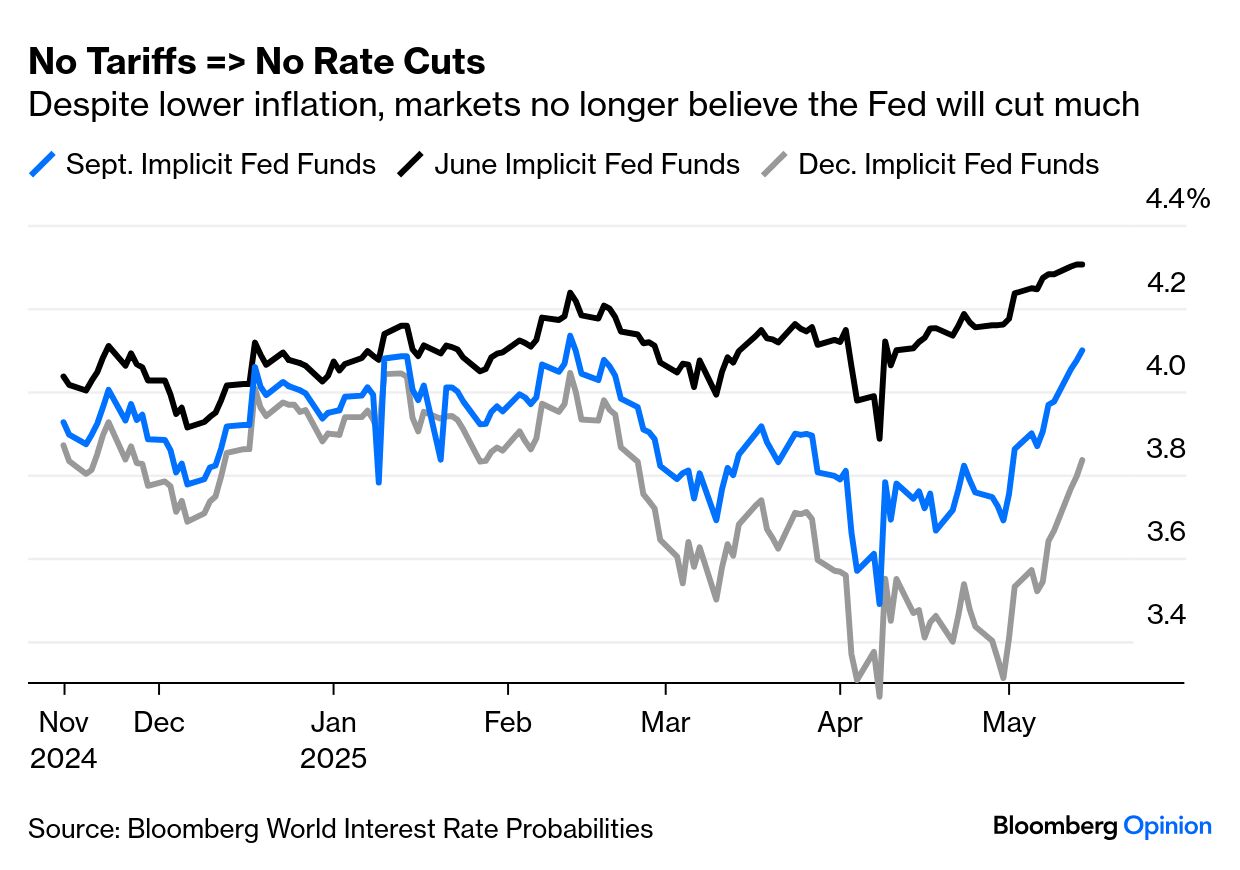

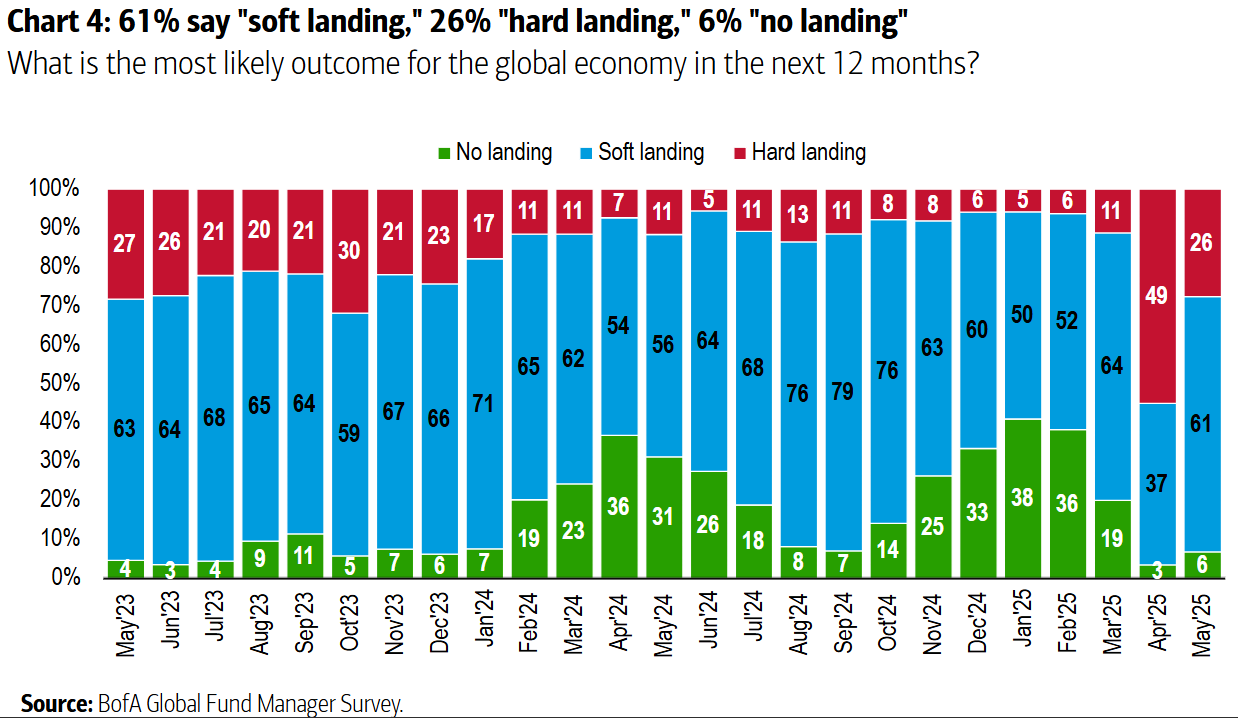

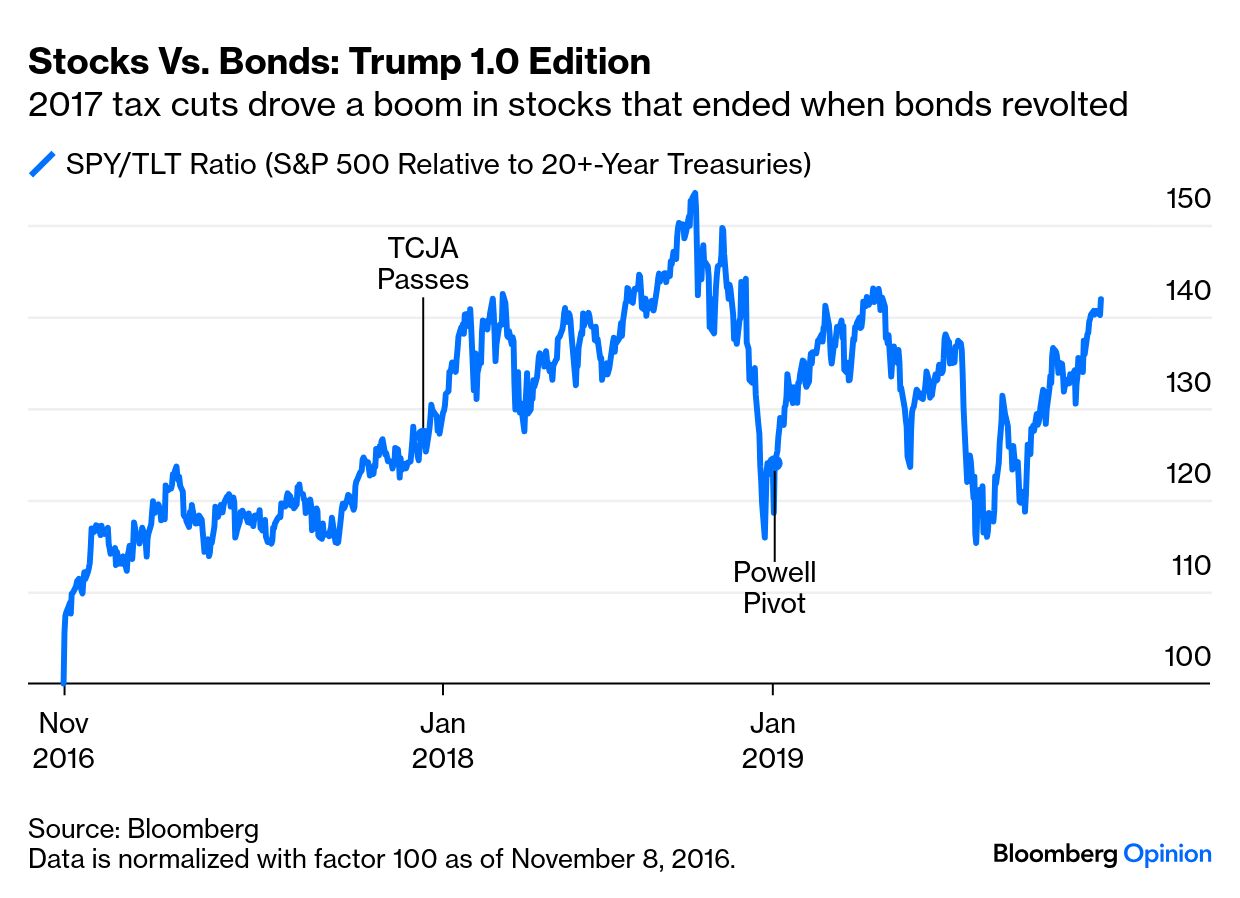

| Donald Trump has a way with words. Nobody can possibly take this away from him. After six weeks dominated by a Liberation Day that was anything but, the debate has moved to the president's promise of a Big, Beautiful Bill that is certainly big, but not very beautiful. The bill has now arrived in Congress. It's a basis for negotiation and is bound to change in important ways before it can become law — but the bottom line is that the combination of tax cuts with feeble attempts at cost cuts will mean a deeper deficit. The Biden administration avoided a widely anticipated recession over the last two years by priming the fiscal pump. The federal deficit has never been this deep outside a recession. Indeed, it hadn't been this serious even during the downturns of the 1970s and 1980s: Until recently, the new administration had appeared ready to take a big hit to its political capital in the aid of reordering global trade. Now, it seems the bond vigilantes may need to levy a similar price to bring fiscal continence back to the US. The menacing rise in longer yields shows that they have doubts: Bonds have moved in conjunction with expectations for the Federal Reserve. Tariffs posed a clear and present danger to US growth. After April 2, when the administration was insisting that trade levies were not merely a negotiating tool, fed funds futures began discounting a series of cuts. That is over. The implicit rate for next month's Fed meeting is at a new high, with the chance of a cut now negligible: Meanwhile, the most imminent risk has shifted from stagflation (a real possibility if tariffs remained at punitive levels) to inflation. Viewing the economy in terms of landings has gone out of fashion of late, and the Bank of America survey of fund managers showed that belief in a "no landing" scenario — in which the economy booms, inflation is not tamed, and rates eventually have to rise still further — almost disappeared during the tariff tantrum. We can expect those odds to rise considerably from here: All of this is consistent with the theory that Trump has given up on a certain kind of 2.0 radicalism, and will now follow his 1.0 model — which involves tax cuts, and a pronounced concern to please the stock market. Eight years ago, that led to a potent rally once it became clear that the tax cuts really were going to happen. It ended when 10-year yields rose to 3.25% — a level that at that point the stock market could not tolerate: The excitement of the savage selloff in late 2018, culminating in what has come to be known as the Christmas Eve Massacre and a pivot toward easier money from the Fed, gives an idea of the risks ahead. It also suggests that investors would be well advised to stay on the equity train while watching the bond market very anxiously. Julian Brigden of Macro Intelligence Partners warned that the administration could shift back to "the devil-may-care policies of Trump 1.0": This shifts the risk from stagflation to inflation and suggests we need to price out any chance of an imminent Fed rate cut. At the same time, we need to watch for signs that the rest of the world is no longer willing to fund our profligacy, as we ultimately search for a level of bond yields that brings stocks to heel.

Will it really play out this way? The DOGE cuts suggested a sincere attempt to reduce the deficit, but were centered on relatively small departments unpopular with core Trump supporters. The bill that is emerging aims for $900 billion in spending cuts from the House Energy and Commerce Committee, which covers Medicaid and Medicare. This would likely go down like a lead balloon with the Trump base, and has already aroused Republican opposition in Congress. Even if that opposition is overcome, Ajay Rajadhyaksha of Barclays points out that the bill "seems to add around $2.5 trillion to the deficit over the next decade.'' Further, claims that the proposed tax cuts will cost "only" $1 trillion rests on the tenuous assumption that they wouldn't be continued: It seems very unlikely that Congress will not attempt to extend these expiring tax cuts right before the 2028 presidential (and congressional) elections – no one wants to tell their constituents that they face a big tax hike right after the election.

What seems to be constant is that it's the bond market that decides. "Yippy" bond yields shook the administration out of its extreme tariffs, rescuing stocks in the process. It may yet fall to the vigilantes to save Washington from fiscal profligacy — only this time, that would involve squelching what is building into a remarkable rally in equities. |

No comments