| I'm Chris Anstey, a senior economics editor. Today we're looking at a new tally of the potential global economic cost of the trade war. Send us feedback and tips to [email protected]. And if you aren't yet signed up to receive this newsletter, you can do so here. - President Donald Trump warned the US economy may slow if the Federal Reserve does not move to immediately reduce interest rates.

- Markets are discovering that the real Trump trade is "sell America."

- Coming up: The IMF is set to downgrade its economics forecasts.

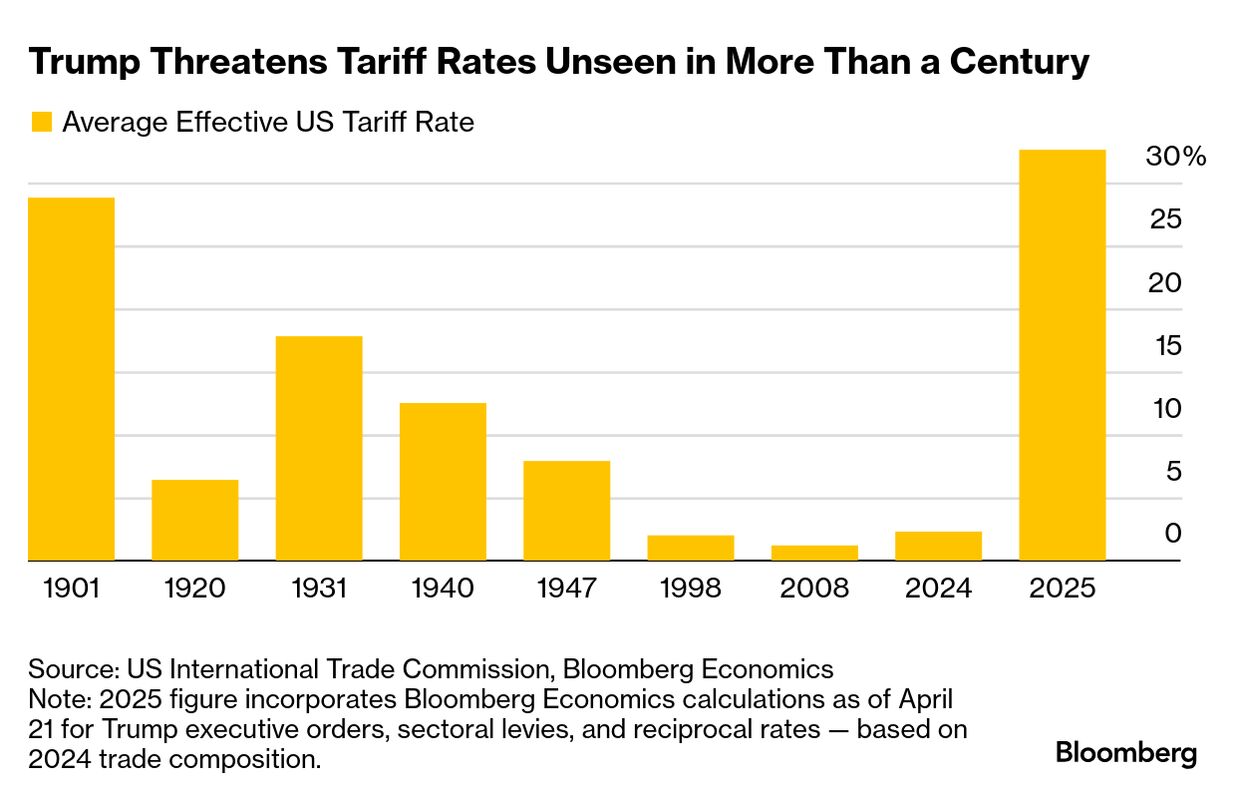

Take historic steps, expect historic reactions, Bloomberg Economics says in its latest analysis of the global economic impact from Trump's tariff program. Trump has often said he thinks trade deals will be made with US partners — this week, he again said he wants a deal with the European Union, for example — but there's been no specific indication compromises are on the verge of being reached. The US president has also suggested he's fine with the welter of tariffs he's proposed, as major federal revenue earners. Incorporating Trump's April 2 "Liberation Day" levies, most of which are currently on a 90-day pause, the BE team, including Scott Johnson and led by Tom Orlik, has lowered its 2025 GDP forecast to 2.7% from 3.1% for the world as a whole. Assuming the bulk of tariffs remain in place, the team expects growth to remain low next year, at 2.8%. In all, the tariff hikes "will shave about $2 trillion off global output by the end of 2027, relative to a scenario where border taxes had stayed unchanged," the economists says. - For the full note on the Bloomberg terminal, click here.

"Policy uncertainty (it's still not clear where tariffs will settle) and modeling uncertainty (the shocks have no precedent in the post World War II data) mean the error band around that forecast is wide," the economists highlighted. Looking just at the US, the new import duties "act like a massive tax hike," and indicate growth for this year will come in at a 0.6% rate, measured comparing the fourth quarter to the fourth quarter of 2024. That's down from a previously projected 1.9%. Since the turn of the century, the only worse years for growth performance than that were during deep recessions — the quick one in 2020 and the prolonged one in 2008 and 2009. It's even worse, by that GDP measure, than 2001, amid the dot-com downturn. Compared with many on Wall Street, the BE team doesn't see quite as bad as an inflationary bump for the US from the tariffs — with the Fed's preferred core PCE gauge rising 3% this year instead of the 2.6% envisioned before the tariff program. Corporate profit margins will shrink, helping to mitigate the wallop to households, the group says. Much as Fed Chair Jerome Powell indicated last week, growth risks are tilted "to the downside," and inflation ones to the upside, the team wrote. The outlook incorporates just one Fed rate cut, in the final quarter of 2025. Don't Miss the Latest Trumponomics Podcast | Economist Nouriel Roubini joins host Stephanie Flanders, Bloomberg's head of government and economics, to explain China's strategy in Trump's trade war. Listen here and subscribe on Apple, Spotify, or wherever you get your podcasts. The Best of Bloomberg Economics | - Corporate America has some room to absorb costs from higher tariffs — how much it decides to cushion the blow will determine how high inflation goes in 2025. At the same time, Trump's crackdown on immigration is expected to slow job growth and boost consumer prices.

- US Vice President JD Vance held trade talks with Indian Prime Minister Narendra Modi in New Delhi to strike an early deal with Washington.

- Bank of Japan officials see no need to change their stance on gradually raising interest rates despite US tariff.

- Megan Greene, one of the Bank of England's most hawkish officials, said global tariffs is more likely to weigh on prices in the UK than it is to stoke higher inflation.

- Prime Minister Mark Carney is banking on factory-built homes to alleviate Canada's housing crisis.

- Read the Big Take for an account of how Trump's agenda is shaped by Russel Vought, not Elon Musk.

Amid Trump's mounting pressure on Fed Chair Powell over the past days, one point of investor discussion has been whether replacing him with a qualified candidate would necessarily be the trigger for selling US assets that many argue. Paul Ashworth, chief North America economist at Capital Economics, says "it might not be disastrous," at least at first. But in the context of rate decisions being made by a panel, Trump would likely need to keep replacing other Fed board members to secure the policy outcome he's looking for, Ashworth wrote in a note Monday.  Trump, right, announces his nomination of then-Federal Reserve Board Governor Powell, left, to become Fed chair, in November 2017. Photographer: Olivier Douliery/Bloomberg "Trump would be forced to go all-out and fire the rest of the Fed Board too" if the interest-rate setting group sidelined the new chair in a bid to preserve central bank independence, Ashworth wrote. "Sometimes it is not enough just to cross the Rubicon, you have to march on Rome too. We suspect that move would go down particularly badly in the markets." |

No comments