| I'm Chris Anstey, an economics editor in Boston, and today we're looking into how the Fed and ECB are set to diverge. Send us feedback and tips to [email protected] or get in touch on X via @economics. And if you aren't yet signed up to receive this newsletter, you can do so here. - Economic data in China showed a mixed picture.

- Germany's economy is now 5% smaller than it would have been without the pandemic and it'll be tough to recover.

- The euro-area's private sector shrank less than anticipated. Separately, France's credit rating was downgraded by Moody's.

Decisions in the coming year taken by the Federal Reserve and European Central Bank are likely not only to affect the outlook for the US and euro-region economies, but also have implications for trade and even politics. A stalling in US disinflation amid sustained solid economic growth has tempered expectations for Fed interest-rate cuts — a conclusion that may be validated on Wednesday, when Fed policymakers publish their updated projections for their benchmark rate. By contrast, disappointing European economic readings have made the case for sustained easing by the ECB. In Donald Trump's first term in office, a wide gap between US and euro zone rates became a frequent irritant to the president, and a trigger for regular bashing of Fed Chair Jerome Powell and his colleagues. Trump blamed a recalcitrant US central bank for driving up the dollar by not slashing rates, undercutting American trade competitiveness that he was trying to revive with tariff hikes. After Trump returns to the White House in January, another divergence between the Fed and its peers may be the cue for more of the same, according to reporting today from Bloomberg's Catarina Saraiva. With the Fed's rate already more than one percentage point above the ECB's main lending benchmark, the dollar has strengthened 5% against the euro this year. The rate gap is poised to widen to more than 2 percentage points next year, according to market expectations, potentially further driving up the greenback — exactly the opposite of what Trump wants. "I wouldn't be surprised if Trump goes after the Fed for not acting in line," said Derek Tang, an economist at LH Meyer/Monetary Policy Analytics. "This time around, the Trump administration is more organized, and so this very organized approach to tariffs and negotiations with other countries is probably going to lead to a more sustained rise in the dollar. And monetary policy is a part of that." The Best of Bloomberg Economics | - The ECB will lower borrowing costs further as the inflation spike of recent years increasingly moves into the rear-view mirror, bringing the 2% target within reach, President Christine Lagarde said.

- China's top leaders have signaled stronger stimulus to help fill a hole in consumer demand. That doesn't mean Beijing will roll out a "bazooka" package just yet, or abandon its factory focus.

- The Bank of England is embracing caution after a year when officials failed to deliver expected rate cuts.

- Brazil's president says interest rates are too high and the responsibility lays with policymakers at the central bank.

- Global poverty will increase if the world doesn't work to maintain a stable and open trading system, World Trade Organization chief Ngozi Okonjo-Iweala said.

- Nigeria's dying ATMs leave a cash-shaped hole filled by agents.

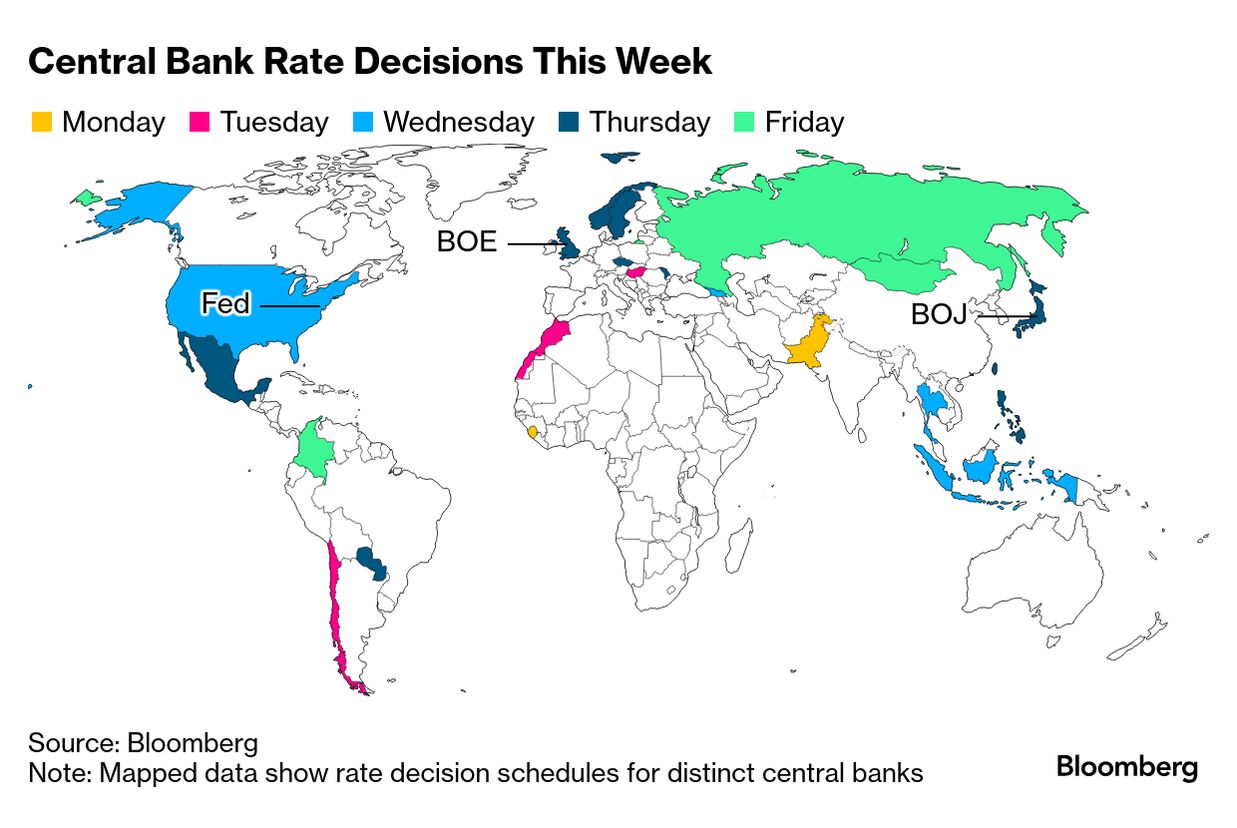

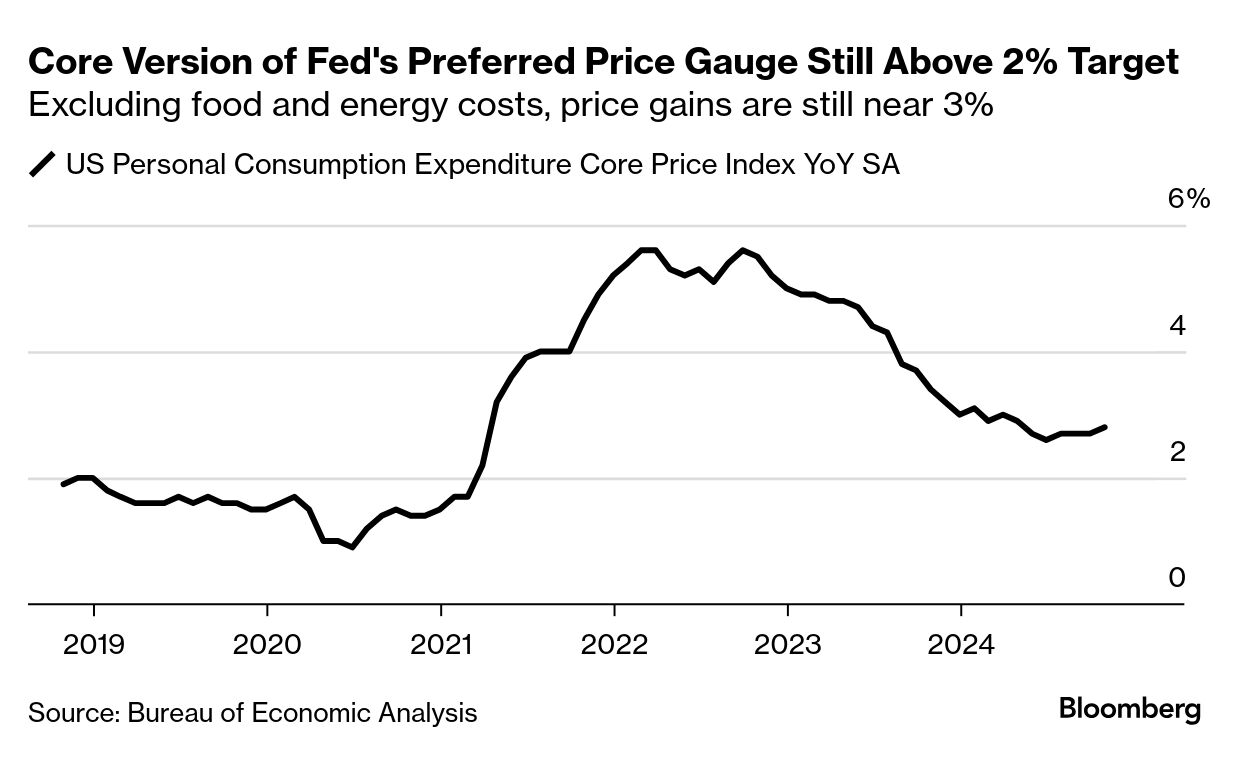

A year when inflation subsided enough for monetary policy easing to start in most advanced economies is about to conclude with a 24-hour flurry of decisions led by the Fed. The US announcement will take center stage on Wednesday, followed by peers in Japan, the Nordics and the UK over the following day — amounting to half of the world's 10 most-traded currency jurisdictions. Those events will draw most attention among investors bracing for the last big week for monetary policy in 2024. By close of play on Friday, at least 22 central banks accounting for two-fifths of the global economy will have set borrowing costs. Elsewhere, key data on the health of China's economy, a likely pickup in UK inflation and business surveys from the euro zone may be among highlights. See here for the rest of the week's economic events. While the consensus view of the latest round of inflation and other key economic figures was that the disinflationary process had largely stalled for now, Citigroup economists expressed confidence that price increases are in fact headed toward the Fed's 2% target. "Home prices have slowed to a typical pre-pandemic pace, wage growth (particularly the Fed's preferred Employment Cost Index) has eased as the labor market has loosened," and the dollar has appreciated, Citi economists including Veronica Clark highlighted in a note last week. They also flagged the price gauges included in monthly purchasing manager surveys were in-line with 2019 levels. "While inflation risks may well re-emerge in the coming years and could structurally remain somewhat above 2%, the end-of-cycle slowing should lead to a period where inflation looks much closer to the Fed's target," the Citi team wrote. They see the core version of the Fed's preferred PCE price gauge ending next year at 2.3% to 2.4% (it was 2.8% in October.) |

No comments