| Bloomberg Evening Briefing Americas |

| |

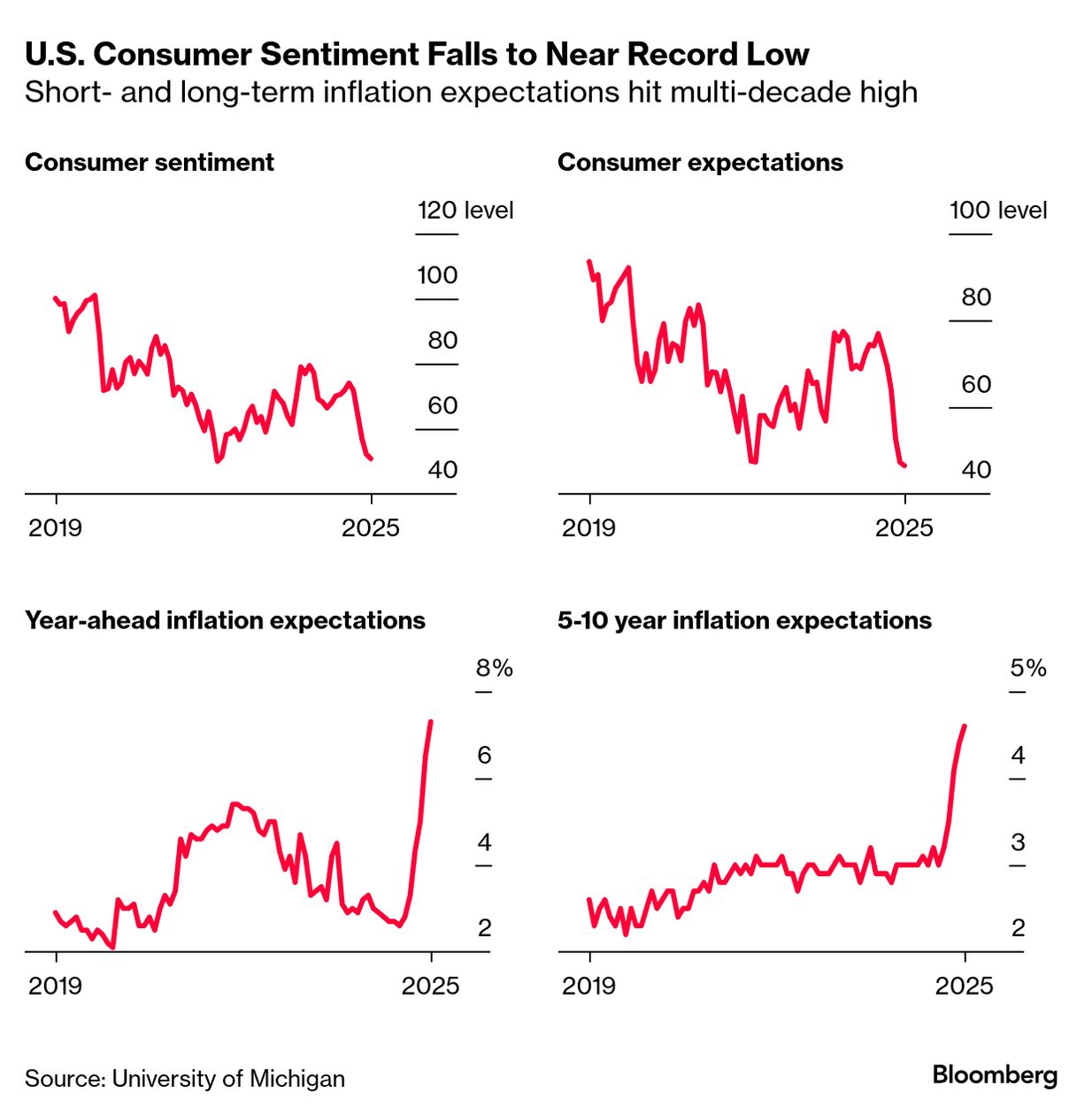

| The US was downgraded by Moody's Ratings on Friday thanks to government debt that's approaching a mind-numbing $37 trillion. It was a dramatic move that cast further doubt on the polarized nation's status as the world's highest-quality sovereign borrower. Moody's lowered the US credit score to Aa1 from Aaa, joining Fitch Ratings and S&P Global Ratings in grading the world's biggest economy below the top, triple-A position. The one-notch cut comes more than a year after Moody's changed its outlook on the US rating to negative. The federal budget deficit is running near $2 trillion a year, or more than 6% of gross domestic product, and Congressional Republicans are pushing through budget legislation that could add trillions of dollars more. "While we recognize the US' significant economic and financial strengths, we believe these no longer fully counterbalance the decline in fiscal metrics," Moody's wrote in a statement. Earlier today, new data showed US consumer sentiment has fallen to the second-lowest level on record, and inflation expectations climbed to multi-decade highs. The preliminary May sentiment index declined to 50.8 from 52.2 a month earlier, according to the University of Michigan. That was lower than all but one estimate in a Bloomberg survey of economists. The main reason cited was President Donald Trump's trade war. Nearly three-fourths of respondents to the Michigan survey spontaneously mentioned tariffs. The topic crosses partisan lines, including a notable share of Republicans bringing it up. The new, sobering survey data comes as inflation data from the Trump administration's Department of Labor has been unexpectedly upbeat, coming in softer than estimates three months in a row. —David E. Rovella | |

What You Need to Know Today | |

| |

|

| A key House committee on Friday failed to advance House Republicans' massive tax-and-spending bill after hard-right Republicans demanded even deeper cuts to healthcare for the poor and disabled. Proposed cuts in Medicaid would be used in part to renew 2017 GOP tax cuts that largely benefitted the wealthy and corporations and fulfill populist campaign promises by Trump to eliminate taxes on tips and overtime. It's incredibly rare for bills to fail at this step in the process, with the committee vote typically serving as a rubber-stamp to the bill before it moves to the House floor. But the Republicans are caught in a bind. With razor-thin majorities in either chamber, they can't pull too much further to the right lest members in high-tax blue states bolt. With midterms next year, they are looking to raise the cap their own party imposed on state and local tax deductions during Trump's first term. | |

|

| |

|

| HSBC Holdings is reorganizing its capital markets and corporate advisory units into a new business as part of a plan aimed at helping Europe's biggest bank grab a larger share of the booming private credit industry. The London-based lender said Friday that it was creating a new Capital Markets and Advisory group to house all of its disparate worldwide financing and investment banking activities under a single management structure, confirming an earlier Bloomberg News report. The latest round of restructuring comes on the back of a sweeping overhaul announced late last year by Chief Executive Officer Georges Elhedery shortly after he took the top role. HSBC is among lenders seeking to step up offerings in private credit, a $1.6 trillion global asset class that's luring more and more players as demand rises. | |

|

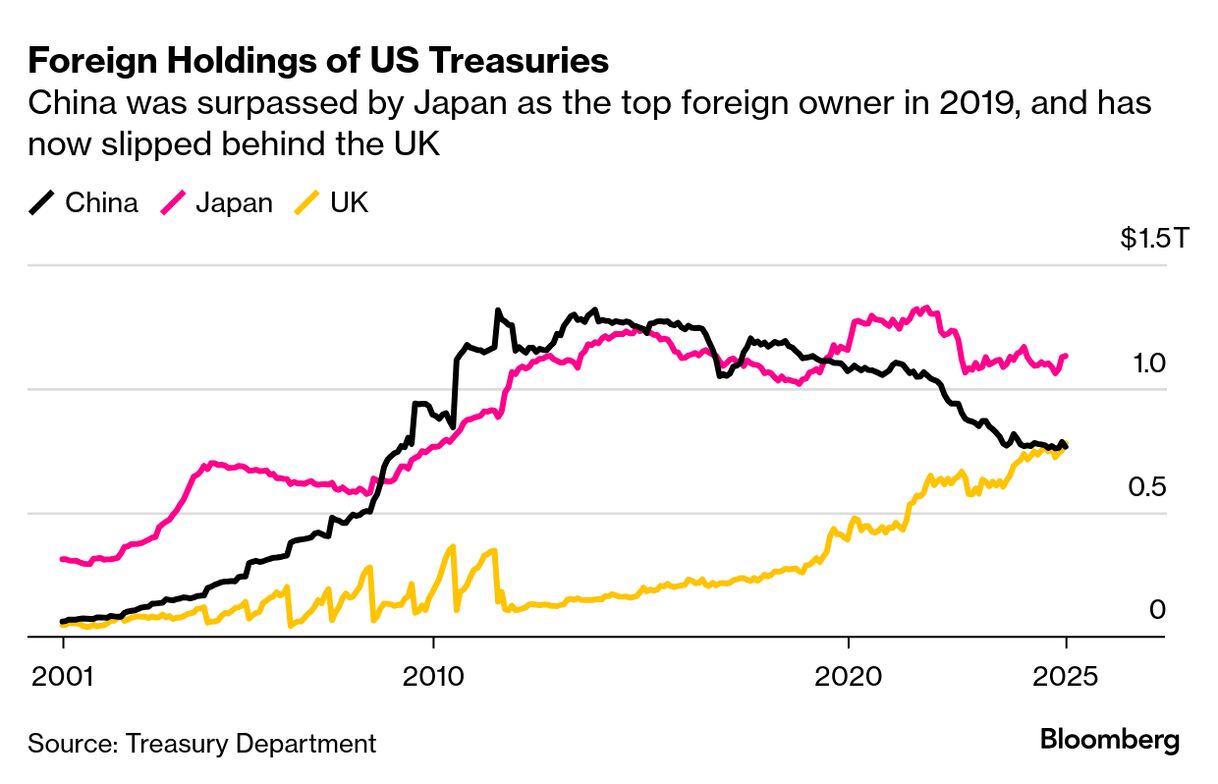

| China shrank its holdings of US Treasuries in March, with the UK replacing it as the No. 2 overseas owner. China was the top holder of Treasuries as recently as 2019, when Japan overtook it. Total overseas holdings of the debt rose $233.1 billion, to $9.05 trillion, Treasury Department figures showed Friday. While the release showed there was no revolt against American government securities in the first few months of the Trump administration, the data predates the destabilization of the US Treasuries market last month following Trump's rollout of "reciprocal" tariffs. | |

|

| Stocks rose Friday as the Financial Times reported the US and the European Union broke an impasse to enable tariff talks, bolstering optimism about negotiations with America's top trade partners. The news comes after the Trump administration announced an agreement with the UK and a temporary truce with China in the trade war. The renewed optimism sent the S&P 500 up 0.7% Friday, with the gauge climbing over 5% for the week. Action in the bond market was muted, though Treasuries saw a third straight weekly drop—the longest slide this year. The dollar rose despite data showing sentiment among options traders is the most negative in five years. Here's your markets wrap. | |

|

| |

What You'll Need to Know Tomorrow | |

| |

| |

| |

| Enjoying Evening Briefing Americas? Get more news and analysis with our regional editions for Asia and Europe. Check out these newsletters, too: Explore all newsletters at Bloomberg.com. | |

| | This newsletter is just a small sample of our global coverage. For a limited time, Evening Briefing readers like you are entitled to half off a full year's subscription. Unlock unlimited access to more than 70 newsletters and the hundreds of stories we publish every day. | | | | | | |

| |

Before it's here, it's on the Bloomberg Terminal. Find out more about how the Terminal delivers information and analysis that financial professionals can't find anywhere else. Learn more. Want to sponsor this newsletter? Get in touch here. | | | You received this message because you are subscribed to Bloomberg's Evening Briefing: Americas newsletter. If a friend forwarded you this message, sign up here to get it in your inbox. | | |

No comments