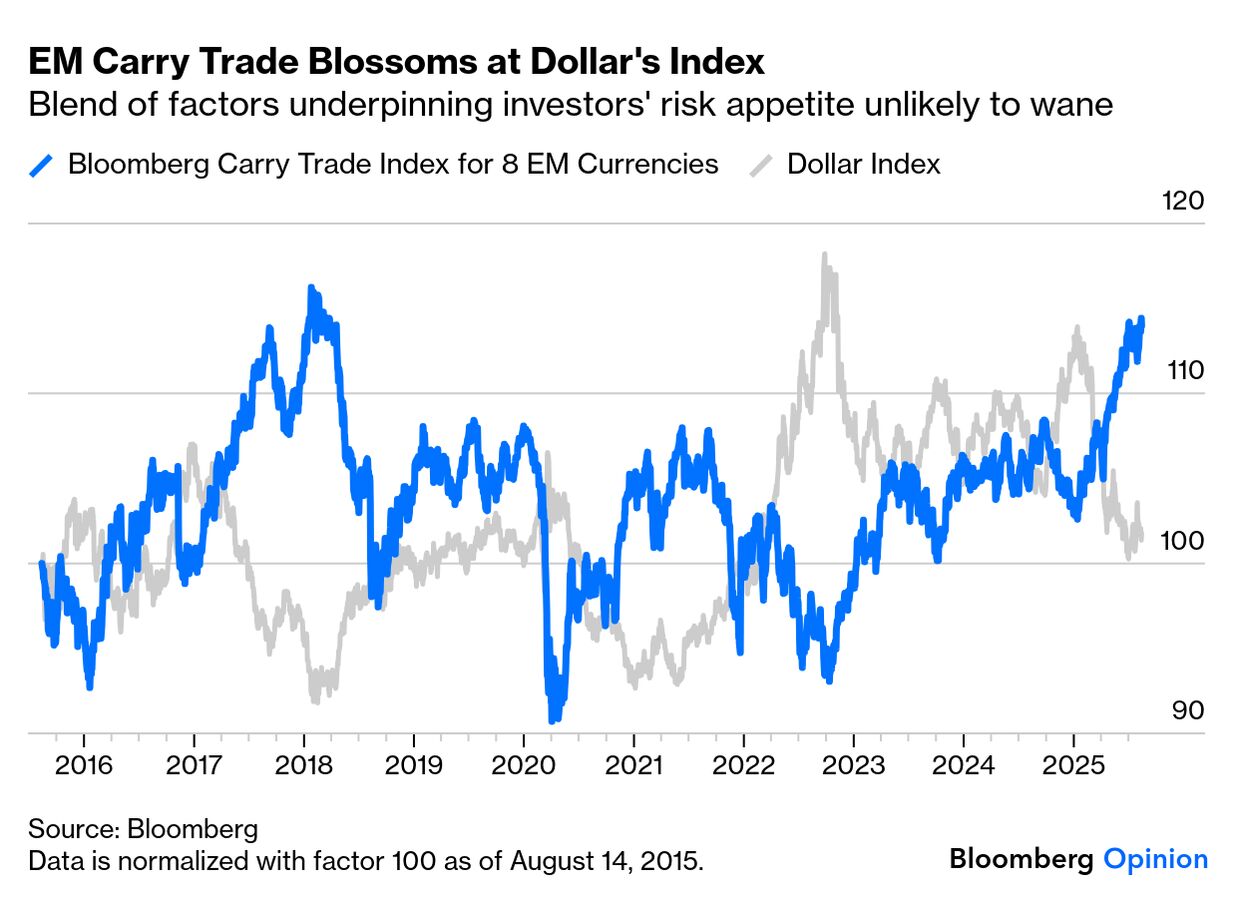

| Carry traders have put last fall's bruising losses behind them and are jumping back in. The struggling dollar has had its worst first-half performance in over 50 years. That means gains in emerging markets, where carry traders are swooping in to cash in on the arbitrage. That is clearest in the traditional carry trade, which borrows in yen and parks in the higher-interest-rate economies of Latin America, led by Brazil and Mexico: Optimism for rate cuts, which seemed a done deal before Thursday's producer price data suddenly reintroduced doubts, continues to fuel the trade. Investors poured about $1.7 billion into global funds dedicated to developing world debt in the week ended Aug. 6, Bank of America said, citing EPFR data. The Institute of International Finance shows that inflows into EM portfolios accelerated in July, climbing to $55.5 billion from $42.8 billion in June. Bloomberg's carry trade index — tracking returns from long positions in eight emerging market currencies financed by short positions in the dollar — has climbed 11% so far this year: Gavekal Research's Udith Sikand argues that this winning streak could continue, and investors playing the trade won't get carried out just yet. The factors boosting EM's appeal, according to IIF's Jonathan Fortun, include resilient macro fundamentals, elevated real yields, and a benign global rates backdrop — which the drama over the Federal Reserve could make even gentler. This has extended a Goldilocks moment for EM. How long it lasts will depend on the Fed: A weaker US growth outlook is ultimately negative for EM, as it can weigh on exports, corporate earnings, and investor sentiment. The key question is how EMs will weather such a slowdown, and this time the challenge is greater given the policy shock from tariffs, the reconfiguration of global supply chains, and the latent geopolitical risk that continues to hang over markets.

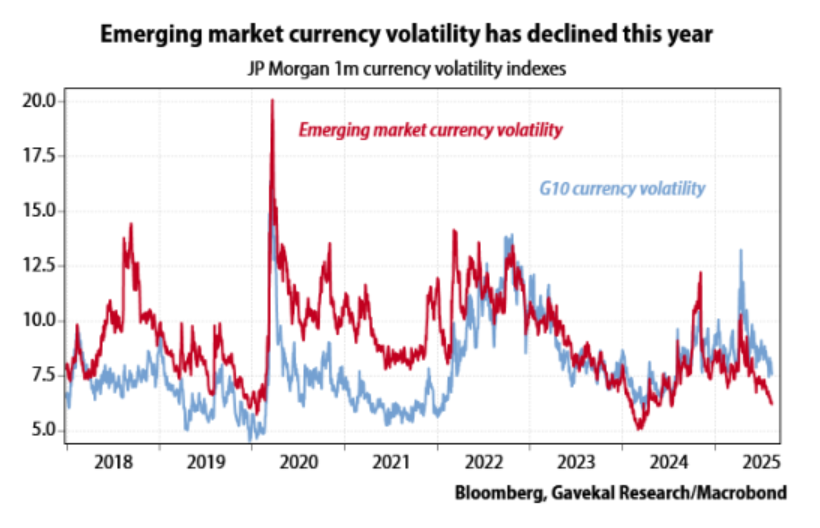

Fortun suggests that current risk appetite rests on the belief that an easing Fed will partially offset softer global demand. That would keep flows alive even as the US economy slows later this year. The potential of tariffs to refuel an inflationary rebound in the US is the greatest risk to this scenario. Still, Sikand observes that despite the tariff uncertainty, exchange rate volatility — the biggest enemy of carry traders — has been relatively subdued. Apart from a brief surge in early April, the fall in emerging currencies has been consistent, as this chart shows: How does that translate into support for the EM carry trade? Sikand explains that this decline in volatility partly reflects the palliative effect that dollar weakness has had on emerging-market financial conditions: Perhaps surprisingly, the effect has proved durable; the reduction in emerging-market currency volatility has persisted even as interest rate differentials have narrowed as central banks in India, Mexico, Turkey, and others have cut while the Federal Reserve has remained on hold.

After last summer's implosion, it's legitimate to question the latest momentum. But Oxford Economics' Ryan Field argues the risk of another unwind is contained as cross-border leverage in the global financial system appears lower than in recent years. The policy landscape remains fluid. US trade policy, adjustments in key EMs, and constantly shifting geopolitical risks could all disrupt this. For now, expectations of continuing strong flows into the EM carry trade make sense; but as we learned last year, they remain vulnerable to any change in the global macro narrative.

—Richard Abbey |

No comments