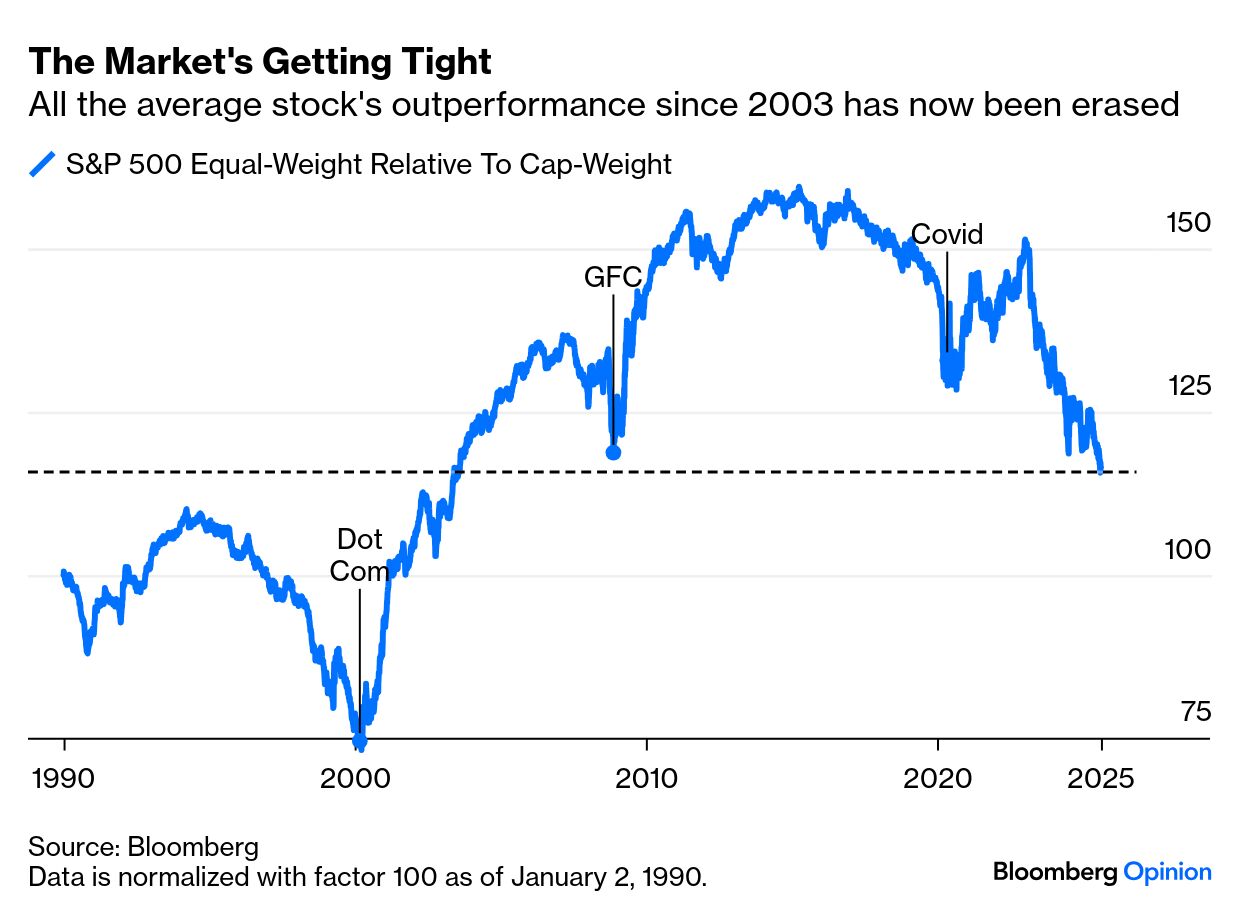

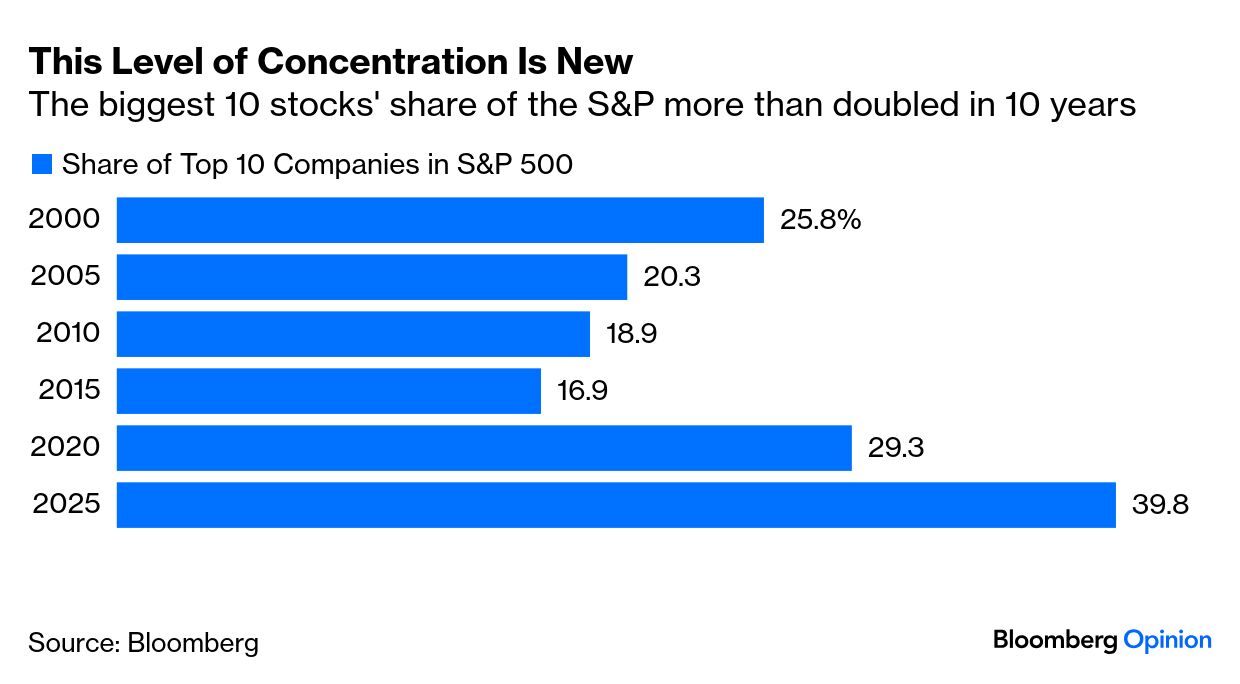

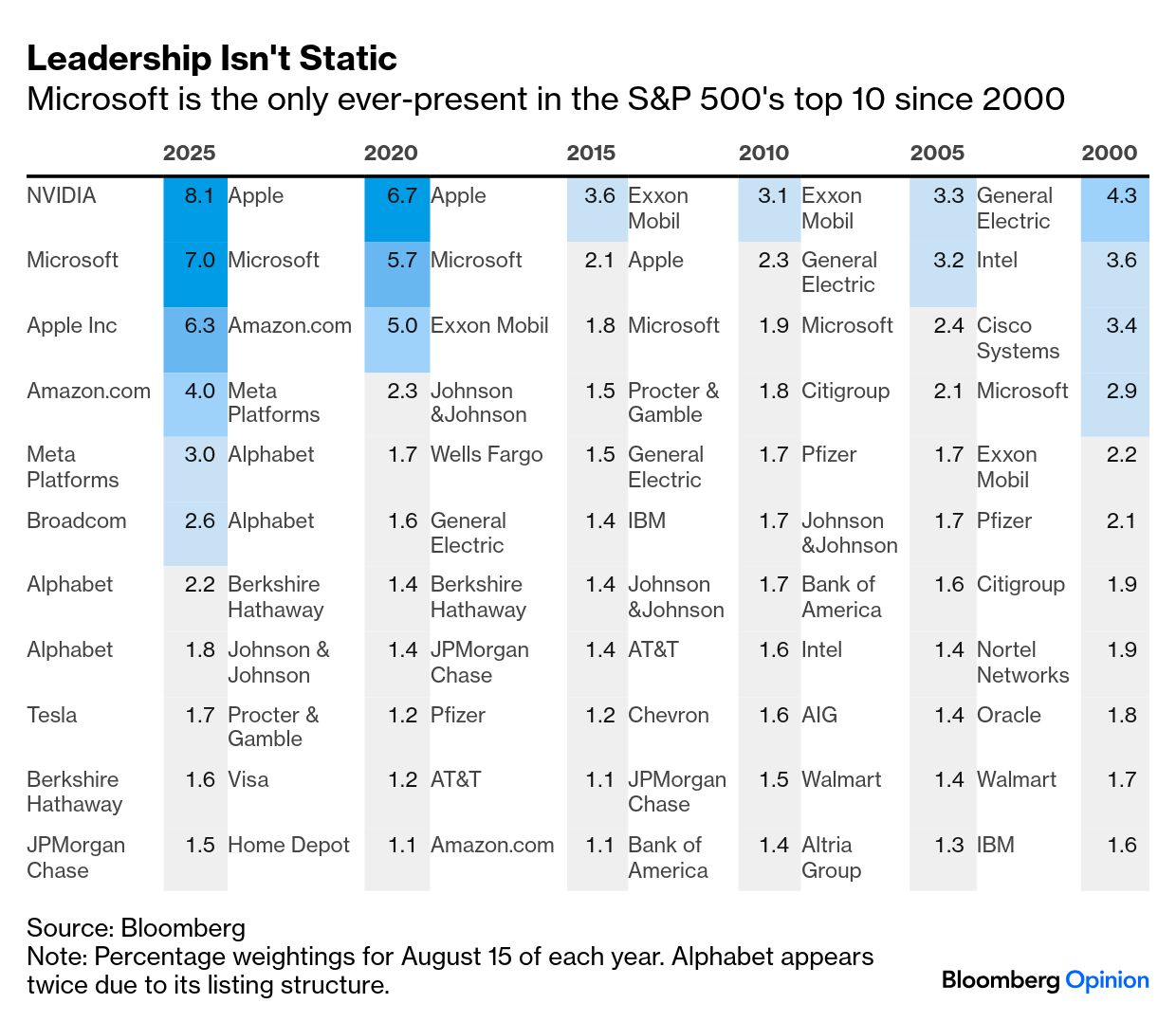

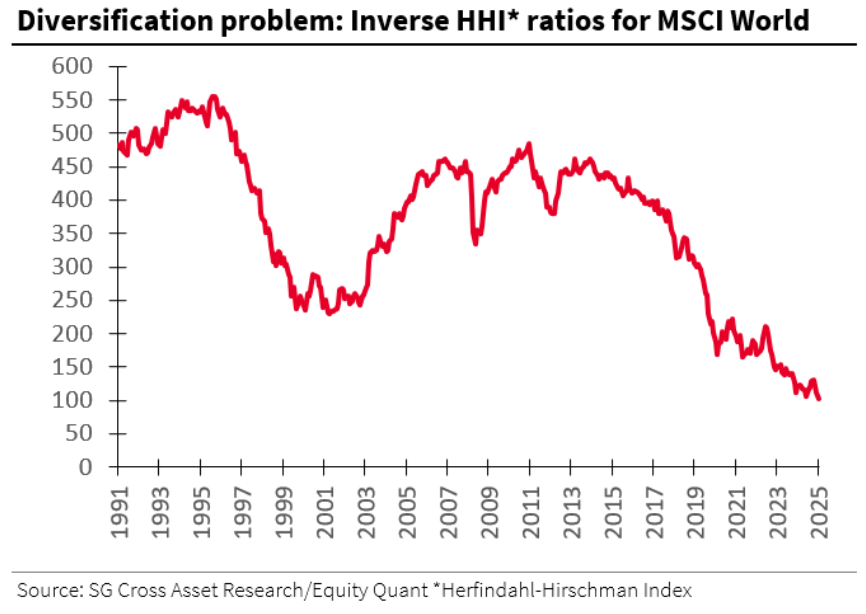

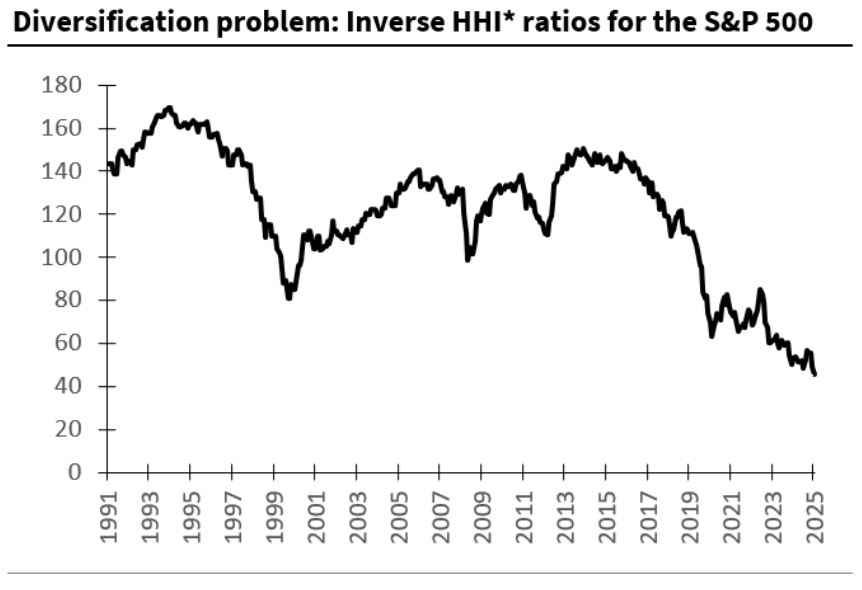

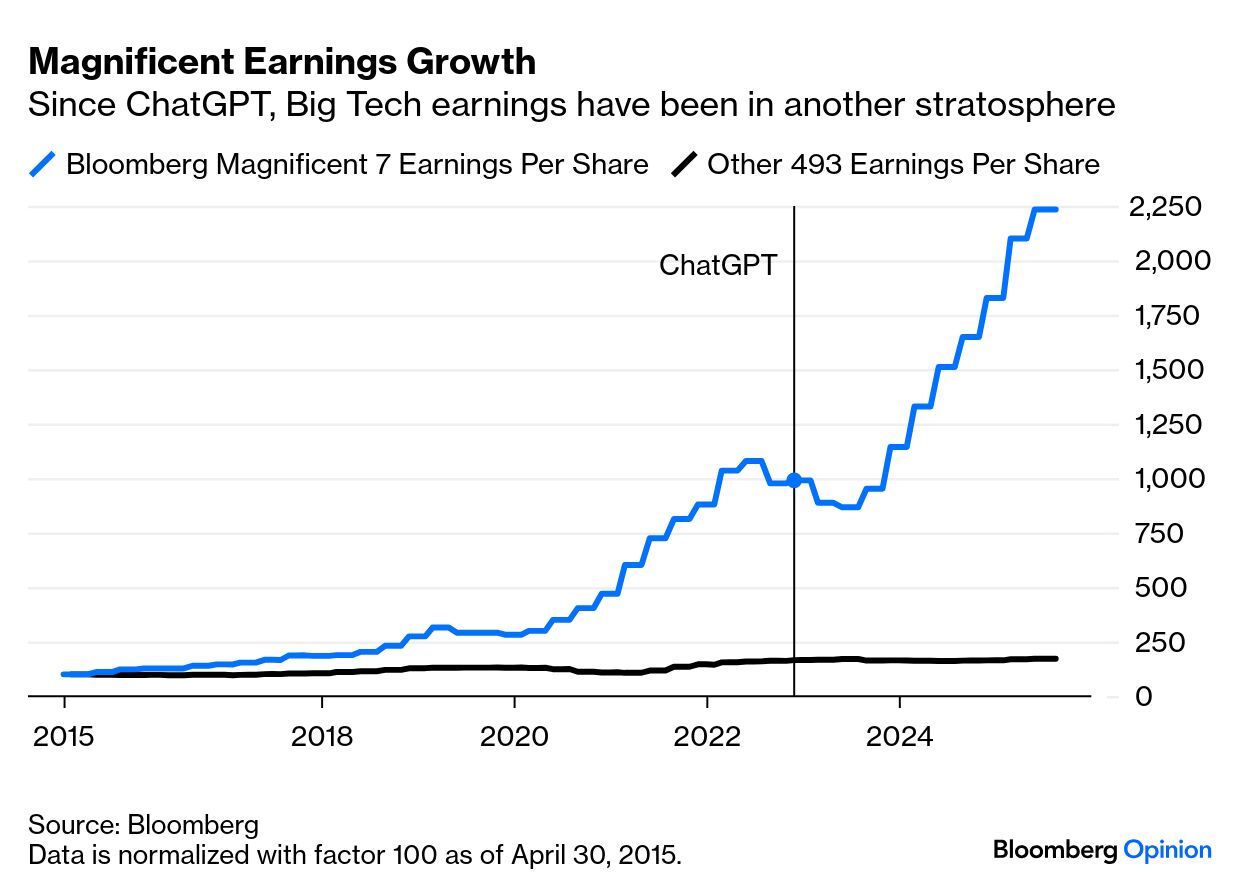

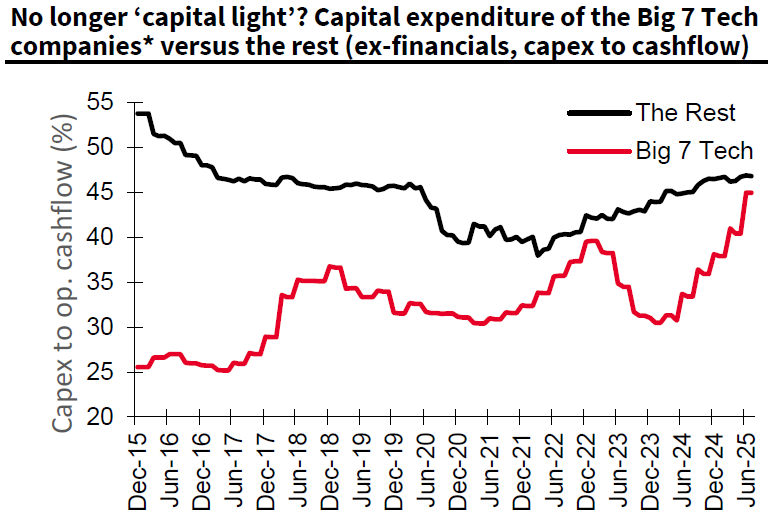

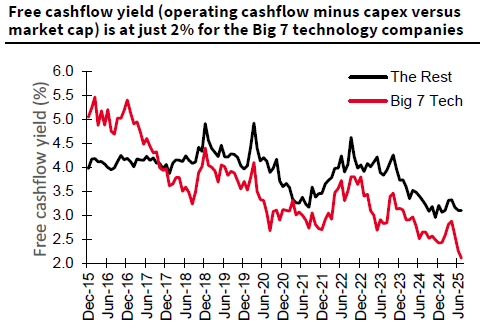

| Newsflash: the US stock market is very concentrated. The performance of the equal-weight version of the S&P 500 — which effectively measures the average stock by weighting each constituent as 0.2% of the index regardless of their size — compared to the cap-weighted index has dropped to its weakest in 22 years: Previous extremes of concentration came with the bursting of the dot-com bubble in 2000, and then with the market crises of 2008 and 2020. This is as tight as the market has become in good times since the internet was taking off. The similarities, with a new technology promising huge gains in profits and revenues, are obvious. For the internet then, read artificial intelligence now. But the dominance of the very biggest stocks is new, and hints at at least one critical difference from the dot-com era. This is how the biggest 10 stocks' weighting in the S&P 500 has changed at five-yearly intervals going back to 2000. It's usual for a few winners to win big at any one time. That's the nature of capitalism. It's unheard of for 2% of the index's companies to account for virtually 40% of its value: It's also unusual for companies drawn from one sector to be so dominant. The Magnificent Seven tech stocks (in which Alphabet counts twice in the chart below due to its listing structure) plus another AI play in Broadcom Inc. take up the first eight spots. That's much greater dominance than in the wake of the pandemic in 2020, or after the internet implosion 20 years earlier: The eagle-eyed will also note that buying the biggest stocks and holding them is a dangerous strategy. Nortel Networks, eighth-biggest 25 years ago, went bankrupt in 2009 and no longer exists. Intel isn't in the shape it used to be. AIG's market cap has shed 80% since its 2000 peak, while General Electric, now on the way back, at one point dropped 92% from its peak. It's really not so unlikely that similar fates will befall one or more of the currently dominant group. That creates a problem for passive investors, as buying the index no longer diversifies risk. These charts show the inverse Herfindahl-Hirschman index, a statistical measure often used by antitrust regulators to measure concentration in industries. It shows the number of stocks needed to match the diversification provided by the index. Now, only 100 stocks are needed to match the MSCI World: Meanwhile, for the S&P 500 that number has dropped below 50: A standard retort to complaints about market over-concentration is: "What does it matter?" It can be a sign of over-excitement about one portion of the market, as was plainly the case during the dot-com boom. But this time is more complicated because the Magnificent Seven stocks have registered very real growth in earnings per share in a way that leaves everyone else far behind. It's hard to say that there's a problem with overvaluation when earnings growth for the Magnificents has outstripped the rest to such an extent: This is not like the dot-com bubble, when hot companies hoovered up cash from investors. This time, a very small group is siphoning profits from everyone else. Rather than the market, the concern lies with the companies themselves. How can they make such big profits, and can they possibly retain them? The big tech groups have also been spending money far faster than ever before. This is a new development. Tech is usually "capital-light." Capital expenditures on the computing capacity needed for AI and the energy to back it have surged, so that the companies now invest almost as much of their cash as everyone else combined: Well-deployed capital expenditures pay for themselves with higher profits, but those still have to happen. Meanwhile, Big Tech's free cash flow yield (operating cash flows minus capital expenditures as a proportion of market cap) leaves little wiggle room for share buybacks or dividends: No end to this trend is in sight. With Nvidia, currently the biggest, yet to report, David Kostin of Goldman Sachs reports that the other Magnificents grew their earnings per share by 26% year-on-year in the second quarter, well ahead of expectations. For next year, their estimated earnings have risen 1% so far this year, while everyone else's have been written down by 4%. According to Kostin, the results prompted analysts to list their Magnificents capex estimates for next year by 29% to $461 billion. History suggests that not all of the Seven will be magnificent a few years from now. It also shows that their current dominance is unprecedented. AI, and their embrace of it, is a phenomenon of the age. All should be aware just how much the current positive perceptions of the market and of the US economy rely on it. |

No comments