|

TACO Tuesday may never come. The conclusion of the three-month pause in the swingeing "reciprocal" tariffs announced on April 2 may not see the expected fireworks after a (not-so) Manic Monday, in which the US kicked the can down the road until Aug. 1. Tariffs are unchanged until then. A Freaky Friday, in the middle of the summer doldrums, awaits.

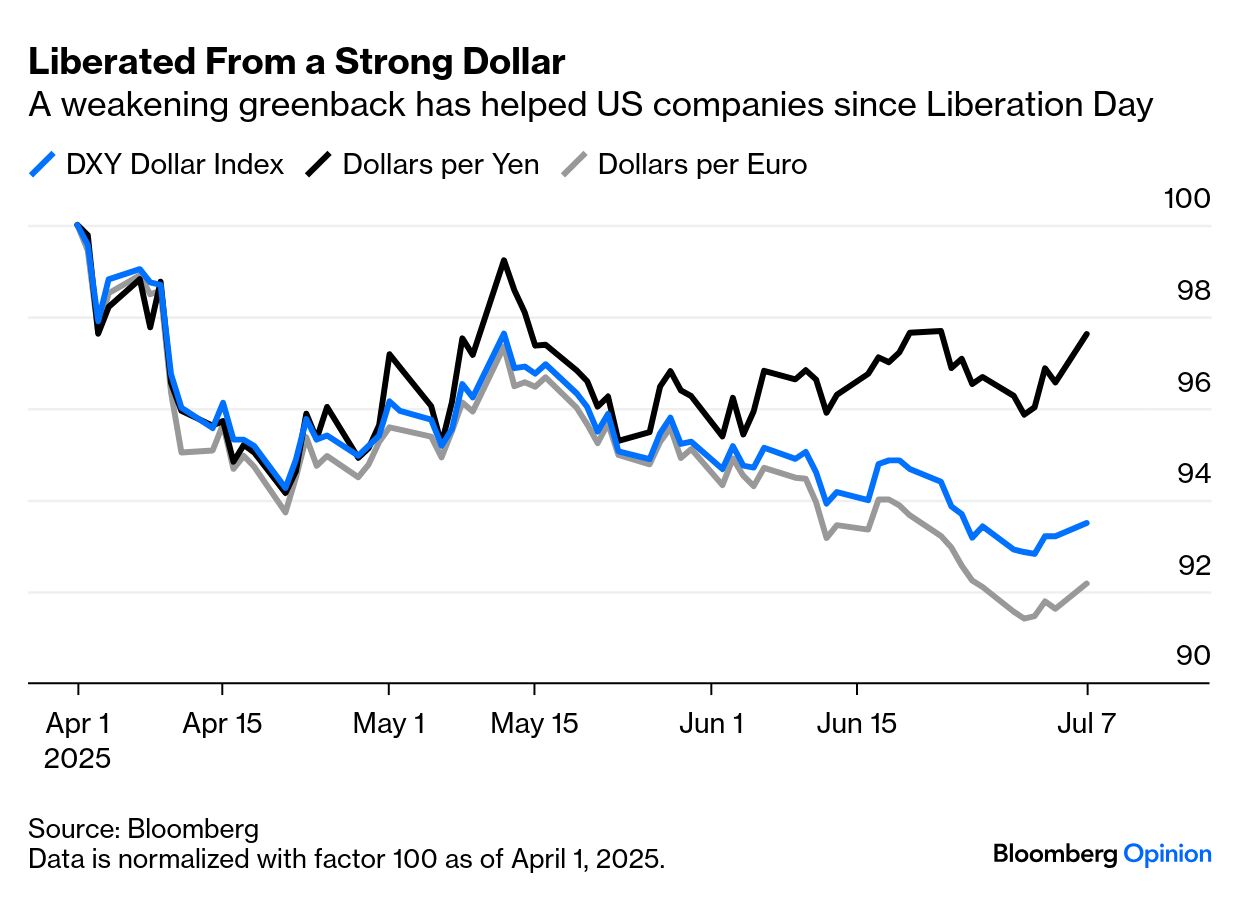

Letters to different countries revealing the proposed tariff rates on their goods that would apply from the end of this month seeped out throughout the day. Most were unchanged from the steep rates announced on Liberation Day, while some were reduced a little. They can still raise eyebrows. Levies of 25% on Japan, South Korea, and Malaysia would, if sustained, surely depress global trade and growth. In all cases the letters, apparently written by the president himself, included a threat to match any retaliatory tariffs, and a hope of reaching a deal this month. It's hard to call this an escalation. Nor is it the full-fledged retreat that some had predicted. That's partly because events in the last three months have strengthened the chances that tariffs stay in force. Since Liberation Day: The Dollar Fell The logic of tariffs is that exchange rates adjust to accommodate them. If levies make US goods more competitive, the dollar should rise to compensate. But the dollar entered the year overvalued, many managers decided to hedge their US exposures, and the currency fell. That boosted US competitiveness: As a weaker dollar is an administration aim, this will be taken as a success. It's harder to tell the president to desist. Nobody But China Retaliated; and Nobody Made a Serious Deal Aside from China, nobody raised tariffs in response (the EU had some levies ready to go when the pause was announced). That reduced the overall chilling effect on global trade. But there were almost no deals, with the exceptions of the UK (as close an ally as the US has, with which it has a trade surplus) and Vietnam. Neither had a lot of detail, or much in the way of concrete concessions. Deals are hard because most countries don't have high tariffs in the first place, while "non-tariff barriers" (like value-added taxes or alleged currency manipulation) are difficult to move. According to Seth Carpenter of Morgan Stanley: Historically, fully fledged trade deals take, on average, three years to conclude, not three months. While history has not been a blueprint for how this year has gone, we still think the lessons are critical, and intense negotiations surround each product category.

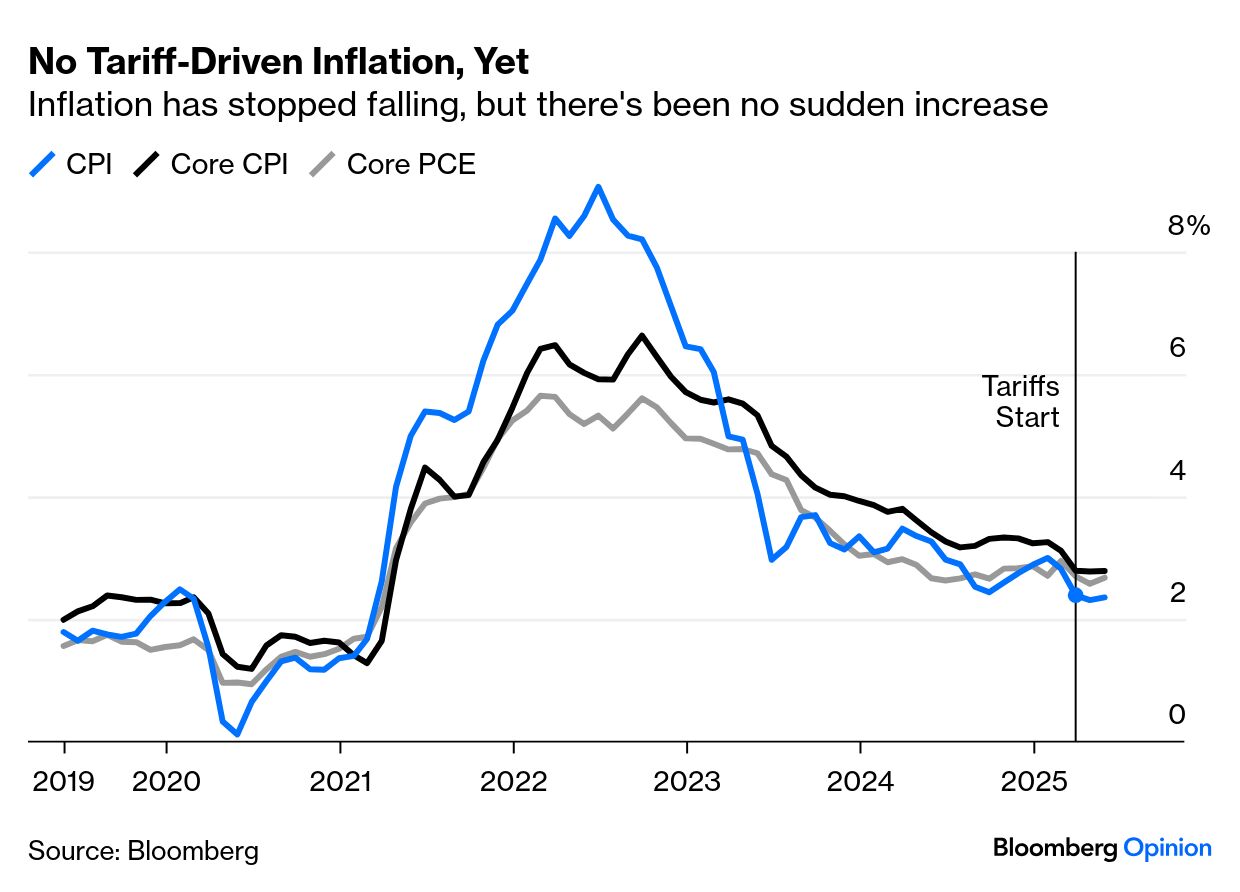

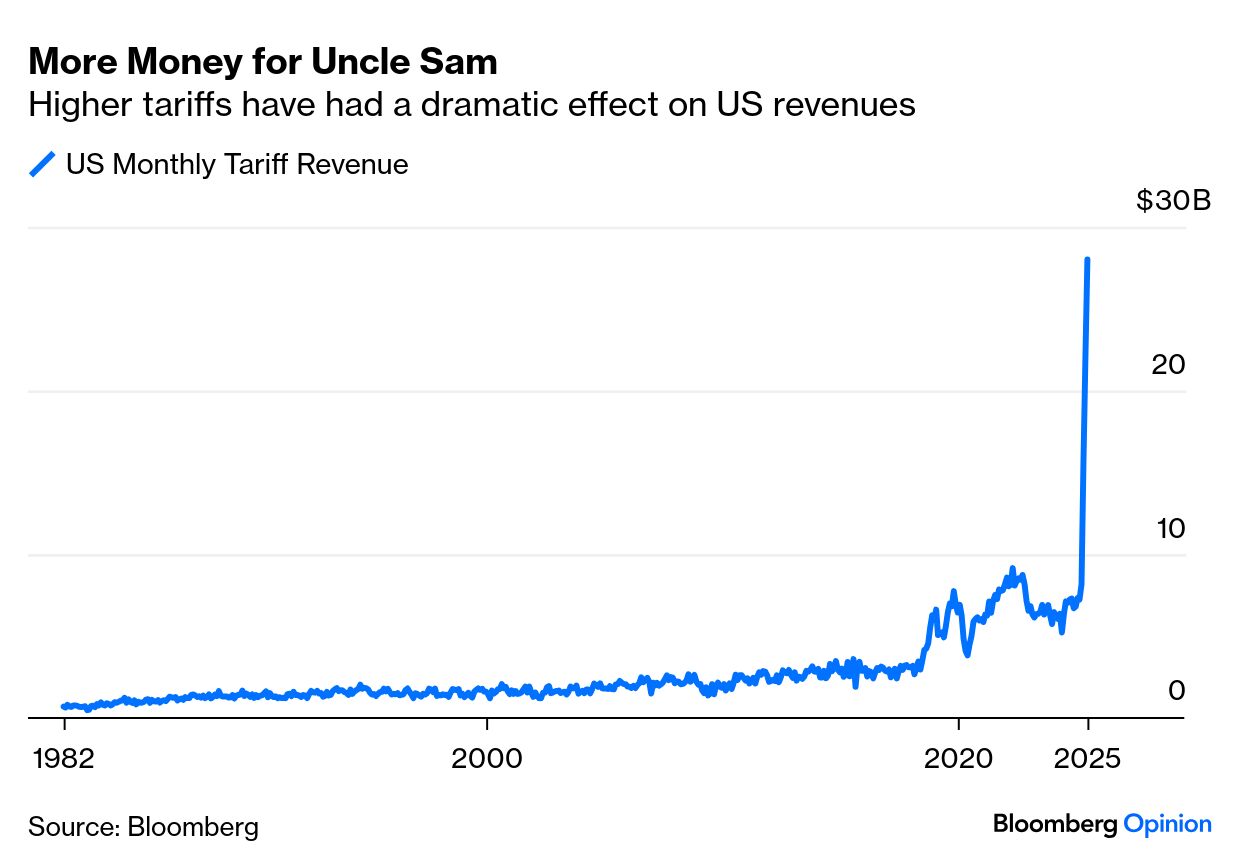

In other words, there's little to no chance that the uncertainty is resolved soon. And there never was much hope of that. Tariffs Haven't (Yet) Made a Big Impact on Inflation or Jobs June inflation won't be available until next week. For the first two months since the Liberation Day 10% baseline took effect, however, signs of tariffs driving price increases were minimal. Unemployment for June, published last week, similarly showed no significant impact from tariffs. It was possible when the 90-day pause started that the data would have enough time to demonstrate that the drive toward protectionism must end. That hasn't happened. As a result, these tariffs may be more durable. Companies Have Paid a Lot of Money in Tariffs to Uncle Sam The tax cuts in the One Big Beautiful Bill Act make revenue from tariffs all the more important. There is always a risk with any tax that a high rate disincentivizes activity and reduces the tax take. That hasn't happened so far: The current baseline 10% rate might eventually prompt a fall in imports — which is, after all, the point of the exercise. For now, the revenue is some kind of a proof of concept. The 10% tariffs are, almost certainly, here to stay. Trump Went on a Winning Streak In the last few weeks, Donald Trump has won massive extra defense spending from NATO allies. He's passed through Congress a sweeping tax and spending bill. Immigrant arrivals have fallen dramatically. The economy is growing, bond yields are low and stocks are at a record. He has bombed Iran, and claimed victory as its conflict with Israel subsides. There are areas where he hasn't claimed a win (the killing goes on in Ukraine), and his victories today might not look so impressive in the long term. But this streak leaves him empowered, and makes the TACO (Trump Always Chickens Out) taunt harder to sustain. It could enable an unembarrassing retreat on tariffs, should he feel the need. But as he's politically strong even after his honeymoon period, it's likely the administration decides that it has more leverage. To quote Tina Fordham of Fordham Global Foresight: No US ally should expect its historic relationship to carry any weight in these negotiations, and the lack of rhyme or reason to the numbers will not give comfort to observers looking for patterns. Trump is riding high post-OBBBA [One Big, Beautiful Bill Act], and this policy highlights his confidence that he "holds the cards."

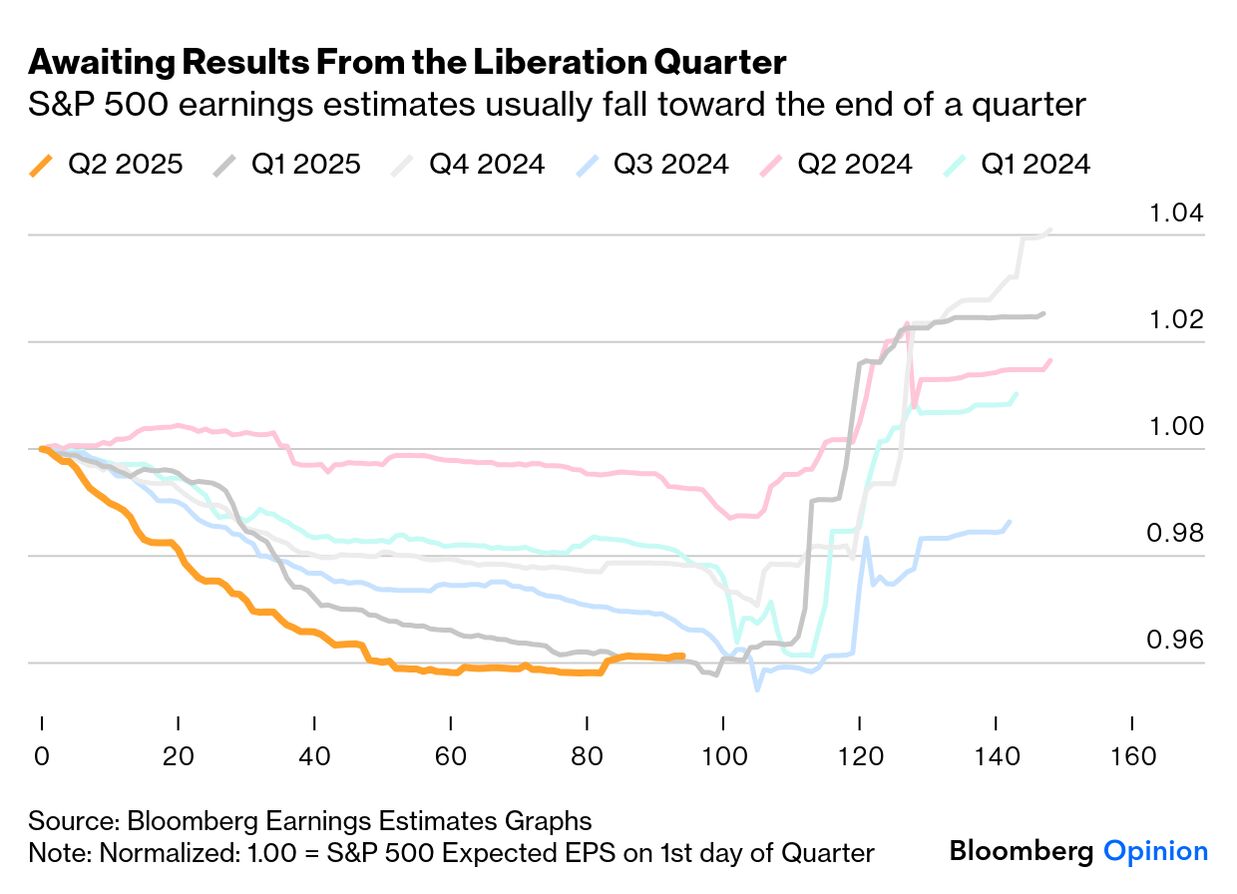

Trump's victories have made a continuing outright trade war more likely. The Impact on Profits Remains Unknown Profits for the Liberation Day quarter will start to appear next week. Tariffs are paid by US importers and should bite into margins. But the weaker dollar counteracts this by raising the dollar value of non-US profits. According to Deutsche Bank AG's Bankim Chadha: Over the prior four quarters, the appreciation of the US dollar was an increasing drag on S&P 500 earnings growth. In Q1, the dollar was up 5.7% year-on-year, implying a meaningful drag, especially for sectors with a large share of foreign sales such as tech and the industrials. In Q2, the sharp decline in the dollar has left it flat y-o-y, implying significant relief compared to Q1.

Earnings expectations for the second quarter fell sharply after Liberation Day — more than in any of the previous five quarters. But the fall is over, and forecasts reported to Bloomberg showed an uncharacteristic slight increase just after the quarter-end: This earnings season figures to be important. Profits will be better than currently forecast because they always are. If they log a surprise on the scale of the last two quarters, that could again be taken as evidence that the 10% baseline tariffs haven't hurt. Donald Trump, who used to run beauty pageants, appears to be modeling this process on Miss World. To amp up the drama, once the contestants had been whittled down to a final seven, those from fifth to second would be announced in turn. The three left would know that they had either won or were unplaced. There's something similar for the trading partners that haven't yet received letters, which include the EU, India, Taiwan, Brazil, Turkey and Australia. Does this mean a deal is coming, or will one of them be hit by an escalation? Australia, with which the US has a trade surplus, might negotiate something positive. India had hopes of a deal. The EU is the most contentious but, according to Politico, believes it can avoid a letter. TACO Tuesday won't be a damp squib if someone makes a deal, or gets hit with escalation. |

No comments