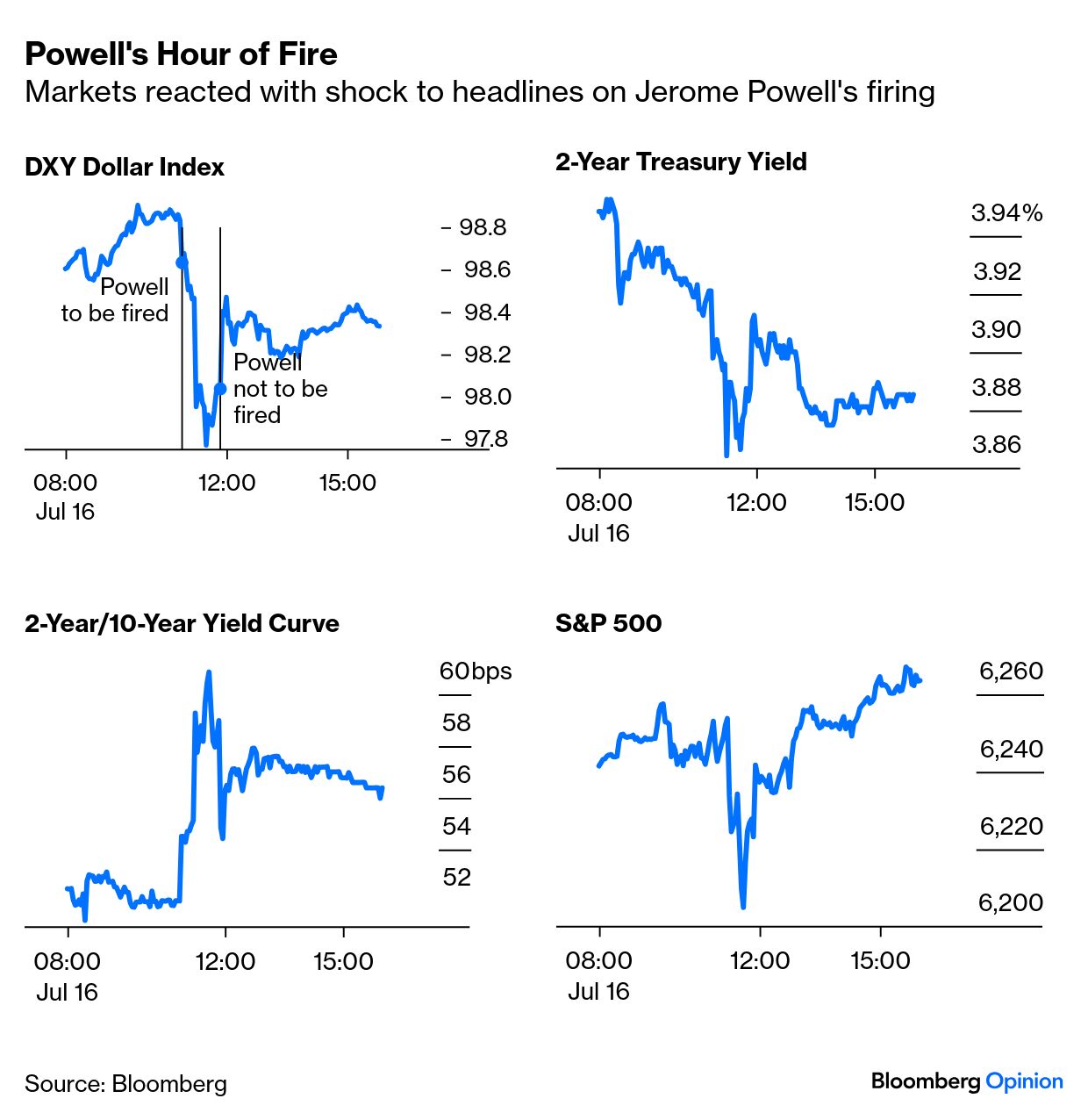

| Schrödinger's Cat won't go away. The famous metaphysical thought experiment keeps coming up in the market. In the conundrum, a cat is in a box with a vial of poison. There is a 50% chance that the poison will be released and the cat will die. While it's in the box and we cannot see it, it is both alive and dead. At this point, the ordeal of Federal Reserve Chair Jerome Powell, who is due to hold the job until May next year, looks very similar. Markets find the situation almost as baffling as the puzzle of the cat in the box. Wednesday morning trading was interrupted by headlines proclaiming that President Donald Trump planned to fire Powell. He had discussed it with members of Congress on Tuesday and shown them the letter he planned to send, as confirmed by a White House official.

An hour later, Trump told reporters in the Oval Office that he wasn't planning to do this. He didn't rule out a firing — and called Powell a "knucklehead" — but said it was unlikely for now. All of this had an effect on markets: From this we can infer that traders hated the prospect of seeing Powell dismissed. But the varying reaction of different assets over the day amplifies the year's market dynamics. Stocks repaired all the damage and ended at a high; two-year yields descended almost to their lows, leaving the yield curve steeper than it had started; and the dollar, which had enjoyed a bounce of late, sustained some damage. All of this makes sense. The administration wants lower short-term rates, and is taking other actions (such as fiddling with bond issuance and shifting bank regulation) to get them. That helps the stock market, and weakens the dollar. A new Fed chairman would push rates down further. Compromised independence would press upward on longer yields, meaning a steeper curve. Because of this, the market consensus has been that Trump wouldn't go through with a counterproductive firing. Matthew Luzzetti of Deutsche Bank AG argues: - It would not guarantee lower policy rates, as monetary policy decisions require a majority vote of the FOMC.

- Government financing costs could actually increase, as bond yields rise as a result of higher long-run inflation expectations and a greater risk premium related to inflation and Fed independence.

- Larger-than-appropriate cuts would likely feed through to higher inflation.

- And Powell's removal could lead to volatility in equity markets.

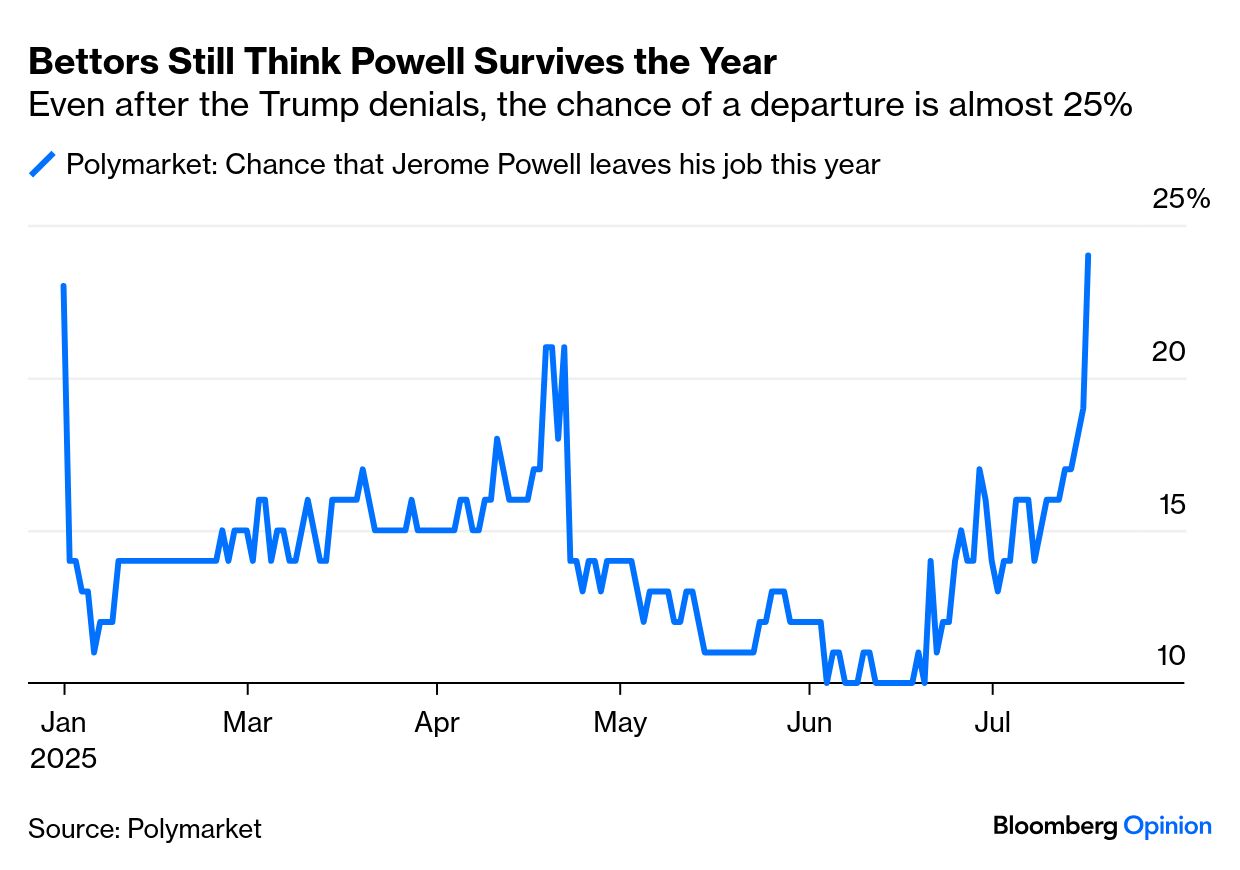

But while this is all true, there's a similar market consensus that announcing massive tariffs would be counterproductive. That didn't stop the president from doing it. By the end of a chaotic morning, it was clear that Trump wanted to undermine his Fed chair — but that he's hesitant to fire him. That raised the odds that Powell departs this year, but it's still a less than a one-in-four chance. This is how the odds have moved on Polymarket: The noise continued. Bill Pulte, head of the Federal Housing Finance Agency, told Bloomberg TV that Powell was "a national nightmare" who was "hallucinating tariffs," talking "nonsense" and "holding back the economy," and would be well-advised to resign. Charles Myers of Signum Global argued that Powell was safe from dismissal until at least after the September meetings, as there are few upsides to firing him now. However, several factors suggest a firing is a real possibility: President Trump seems to "genuinely" believe the country would be better off with a different chair in office. By issuing trial balloons like today's, the president is likely not just testing the market's reaction, but also and more importantly attempting to socialize the idea of Powell's dismissal, such that it may be more easily digestible if and when it does materialize.

Like Schrödinger's cat, Powell's chairmanship lives and dies simultaneously. Another lesson from the day is that the Trump administration continues to be much less constrained than many had assumed (or hoped) it would be. Congress and the courts aren't putting up much opposition, and neither are markets. The infamous TACO (Trump Always Chickens Out) trade is on wobbly foundations. Viktor Shvets of Macquarie argues: Since Liberation Day, investors became convinced that capital market and electoral constraints are sufficiently strong to force the administration to move away from the most destructive policies, and therefore, lack of "adults in the room" is not as frightening as it sounds. While there is some truth in this statement, the degree of consistency with which the US persists in returning to original ideas implies that constraints only reduce short-term intensity, but do not alter the direction or the final destination.

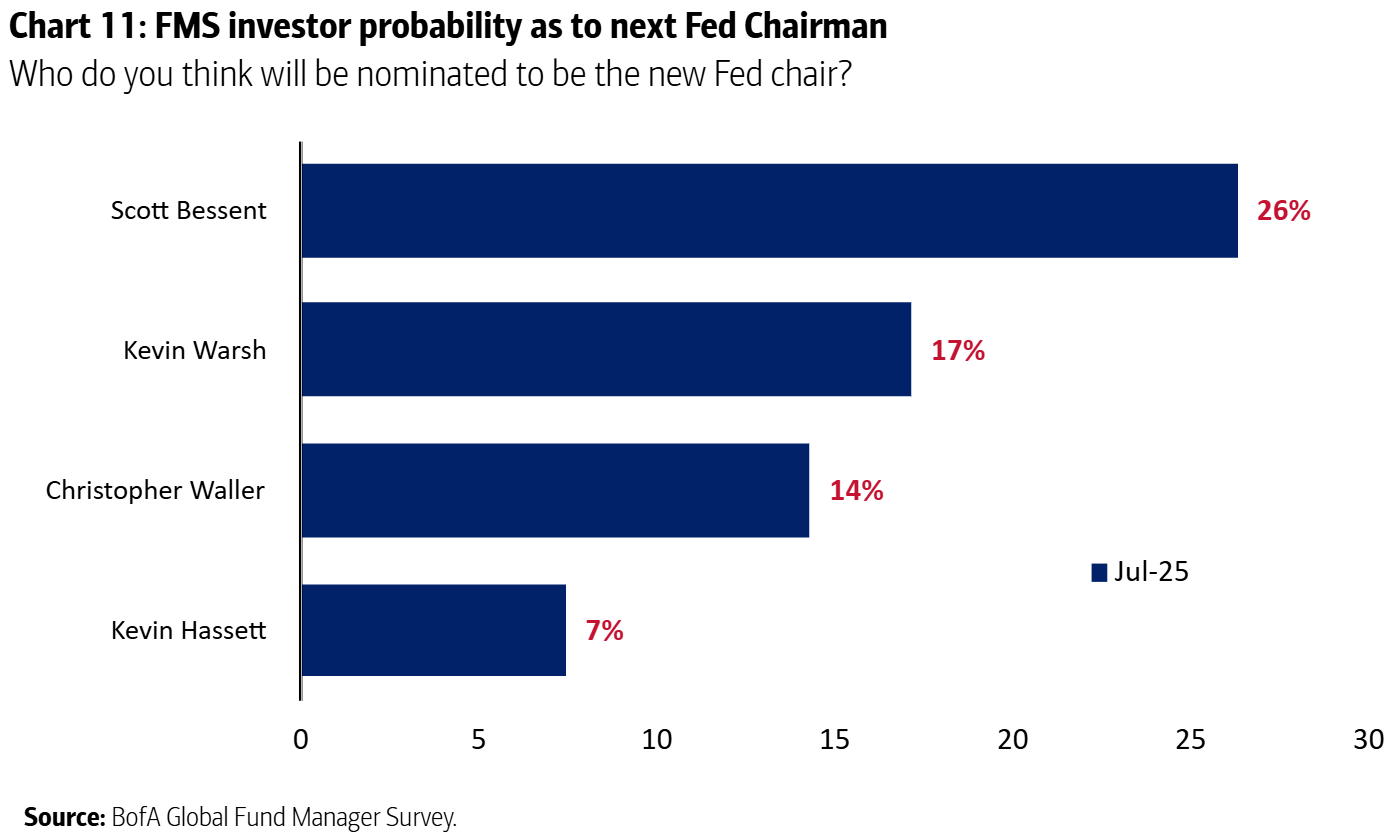

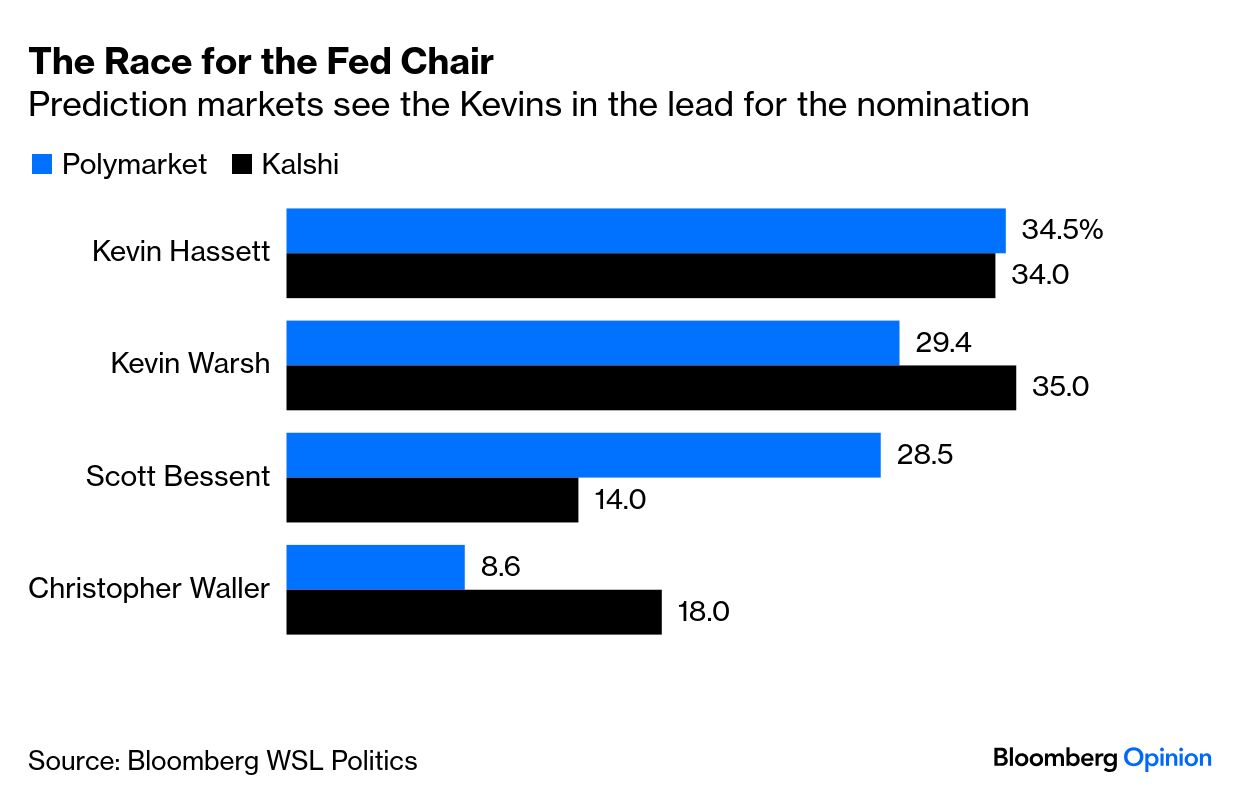

On tariffs, as on Fed independence, the direction of travel remains clear despite the reversals that gave rise to the TACO nickname. The lack of a negative market reaction this time empowers the president further. Or, in another metaphysical puzzle, when the market signals that it's OK with what Trump is doing, the TACOs don't exist. My friend and former colleague at the Financial Times Rob Armstrong came up with the TACO moniker three months ago, and now adds the Taco Paradox: "The less the market believes Trump's threats, the more likely they are to be true." This is his illustration: Wish I'd thought of that. Trump has already nominated one Fed chairman, whom he now calls a knucklehead and a stiff. Despite this, there are plenty of candidates to succeed him. At one level, it doesn't matter who wins. On the positive side, all the candidates in the frame are well-qualified, known quantities, so nothing scary there. On the negative side, Trump makes clear that the winner must promise to slash rates, which limits freedom of action and independence, and makes for a less effective central banker. That said, the conversation is already intense. When Bank of America asked global fund managers for their predictions earlier this month, about a third didn't offer an opinion. The others broke this way, seeing Treasury Secretary Scott Bessent as the most likely: Meanwhile, prediction markets entered the Wednesday mayhem viewing it as a two-horse race between Kevins: Hassett (of the National Economic Council), and Warsh (who served as a Fed governor during the Global Financial Crisis). Christopher Waller, a current governor appointed by Trump, is seen as the most viable inside candidate: All have long track records. Warsh, in particular, has been hawkish in the past. But their ideas and experience won't mean much in the eyes of the market if they must promise to cut rates to get the job. That's what's in prospect. |

No comments