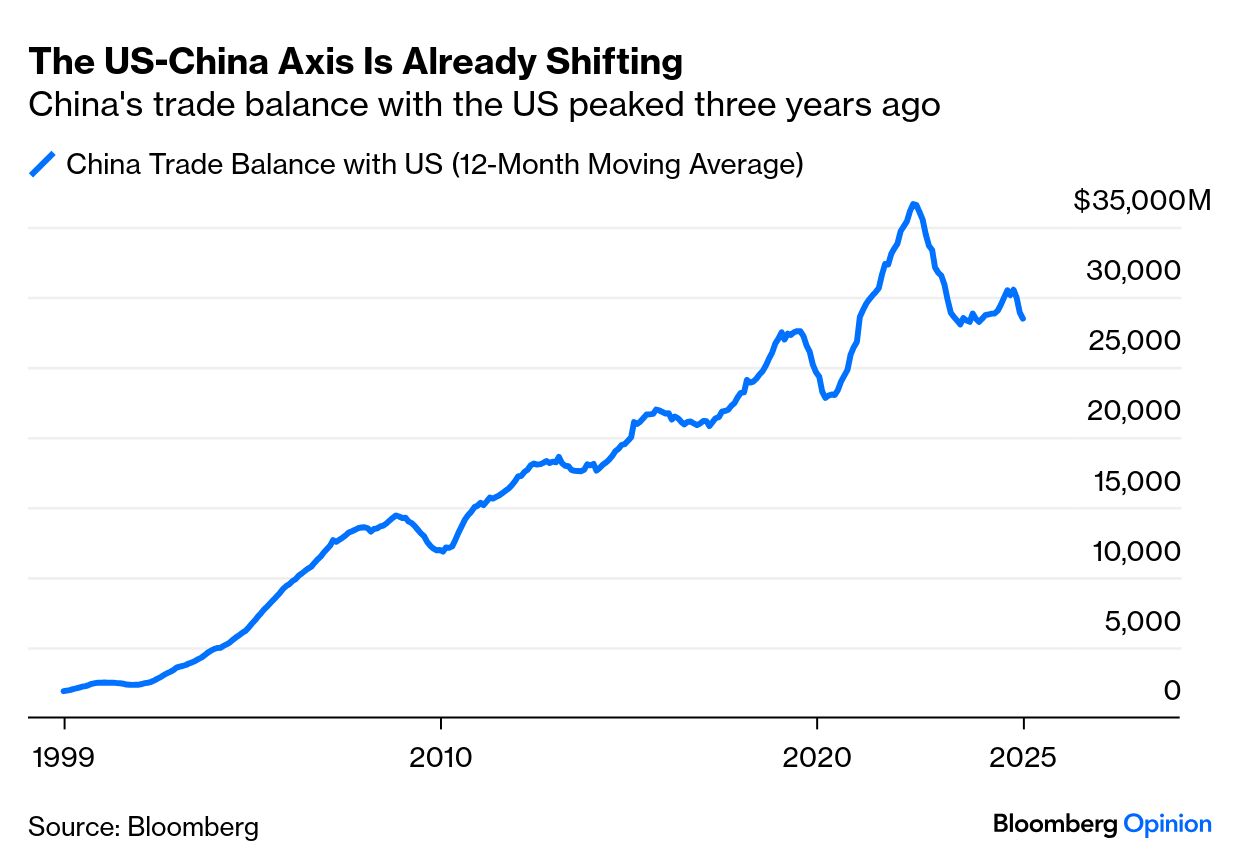

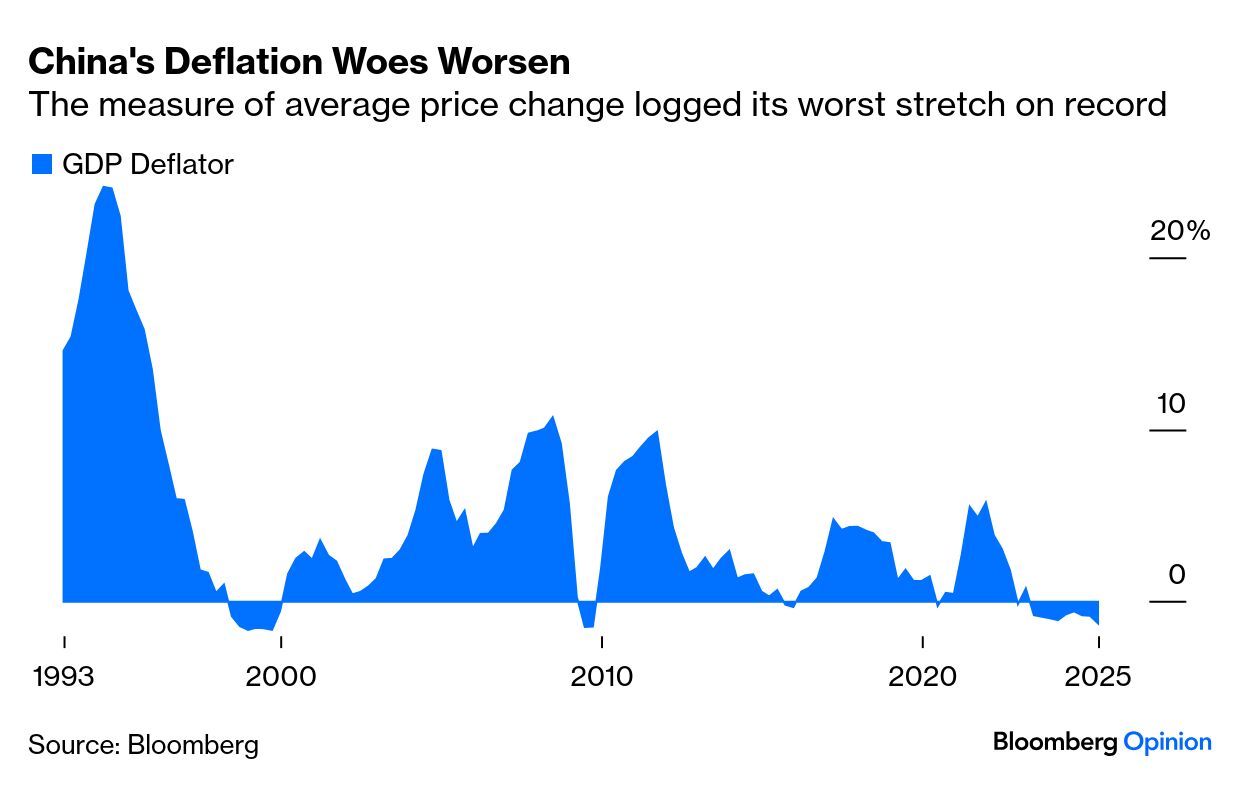

| Beijing's economic growth story is showing a fragile resilience in the face of growing global efforts to "de-risk" from China. Second-quarter gross domestic product growth was modestly lower than its previous advance, but remains on course to meet an ambitious year-end growth target of 5%. Exports continue to be the driver despite tariffs. That underscores the fragility of this expansion, especially as the property sector's problems drag on. A breakdown of the export data shows cracks are forming. US shipments shrank by $35 billion year-on-year in the second quarter. China's trade balance with the country peaked in 2022: However, exports to regions such as the European Union, Africa, Asean, and North Asia made up for the shortfall and brought the last 12 months' exports to a new record: That suggests that the trade realignment Beijing seeks is happening, but policymakers must be prepared for trade-offs. Oxford Economics' Louise Loo notes that price discounting is eroding China's terms of trade and intensifying disinflationary pressures. That has now turned into outright deflation. The GDP deflator, which tracks average price changes over time, fell 1.2% year-over-year in its ninth consecutive quarterly drop. That's the longest streak since records began in 1993, and the sharpest since the Global Financial Crisis year of 2009: Turning this around will take more than exports. Further, US importers are building stockpiles while the US-China trade truce lasts. That could weigh on exports later this year — a risk that policymakers can't afford as Washington pushes on with tariffs. Attempts to boost domestic consumption have largely failed to deliver, with retail sales now slowing down. As Gavekal Research's Wei He observes, softening domestic demand will force the question of whether incremental stimulus is justified. Policymakers at this week's Central Urban Work Conference, the first in nearly a decade, reinforced speculation that imminent help for the property sector may not amount to much: The meeting communique called to "steadily promote the renovation of urban villages and dilapidated housing," but said that China is shifting to "a stage in which the focus is on raising the quality and efficiency of the existing stock" — comments that do not imply a major stimulus in the offing.

Regardless, Oxford's Loo expects housing to feature prominently at this month's Politburo meeting. Without immediate policy help, the slump continues: Given the structural and demographic headwinds, we expect any property easing in the second half to be measured rather than aggressive, given that there is no fundamental or demographic basis for stimulating a housing demand upswing in China.

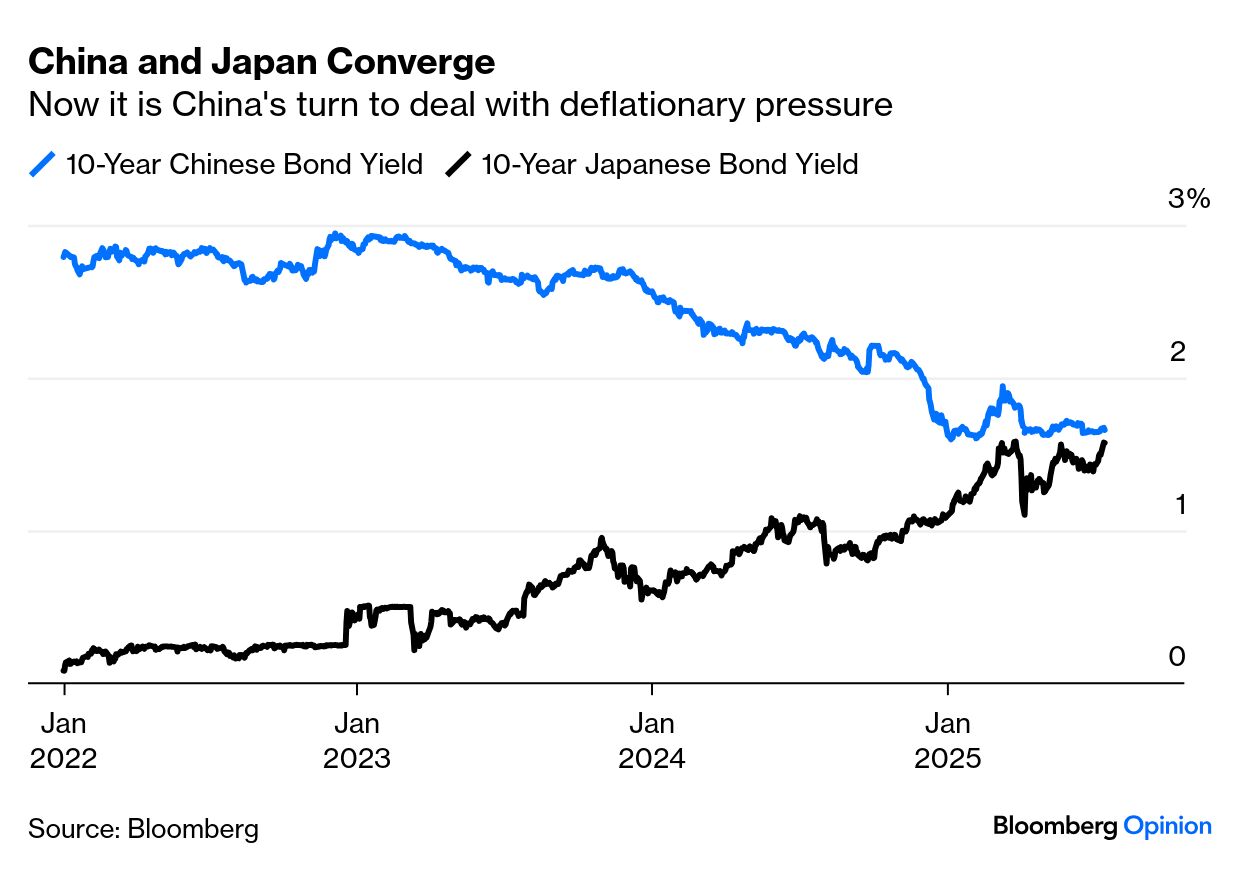

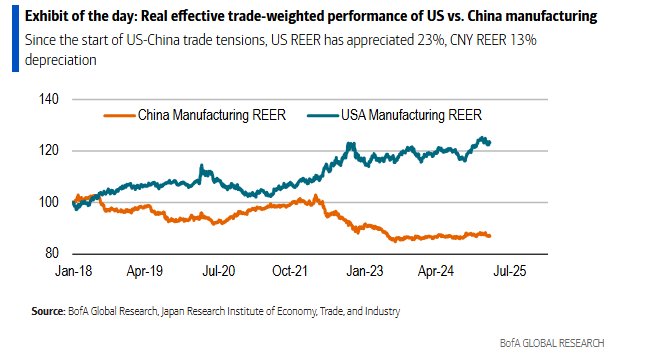

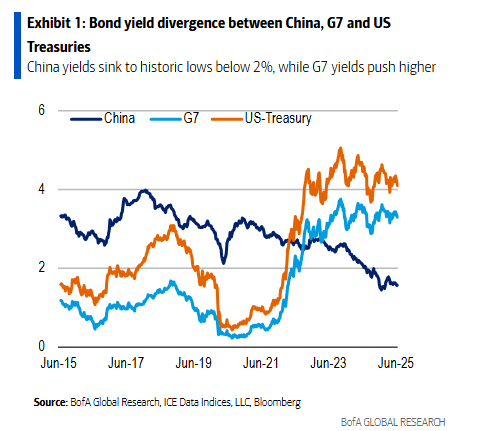

China's earlier efforts to rein in credit help explain nominal yields' fall close to historic lows. The moment when they dip below those of Japan, long gripped by deflation, grows nearer: Bank of America's Claudio Piron observes that Beijing's approach has had the unintended consequence of disinflation relative to its trading partners. Since January 2018, this has caused a real trade-weighted appreciation of the dollar for the manufacturing sector, and a depreciation for the yuan equivalent: The irony, as Piron notes, is that this is exactly what the respective manufacturing sectors don't want — the US is trying to boost manufacturing exports, while China aims to shift toward greater domestic consumption. Further, a divergence in their response to Covid, fiscal stimulus, housing cycles, and now tariffs have added up to higher and steeper nominal yields in the US and lower, flatter yields in China, as illustrated in this BofA chart: As real rates are still positive, thanks to deflation, low yields may not help China's growth that much, and that raises concerns over the sustainability of its debt dynamics. —Richard Abbey |

No comments