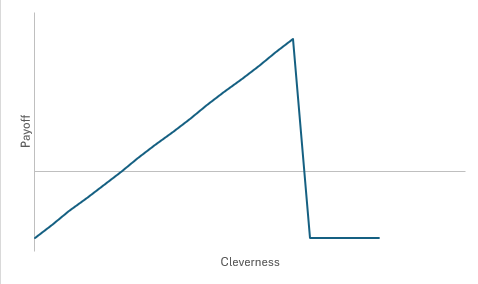

| When an investment bank sells a derivative to customers, the derivative will generally have a payoff graph explaining what the customer will get in various scenarios. But the generic payoff graph for the bank will look something like this: If you sell clients something dumb, you will lose money. If you sell them something clever, you will make money. If you sell them something very clever, you will make a lot of money. If you sell them something too clever, you will make even more money, but then you will have to give it all back and then some. If your clients completely understand what they are buying, there is some cap on how much you can make. But if they completely misunderstand it, you're in trouble. They have to understand it a medium amount. You have to tailor the products to the customers, so that each customer is buying products that are just slightly beyond its capacity to understand. We talked a couple of months ago about some conditional target redemption forwards that UBS Group AG sold to some foreign-exchange customers. This is a fairly complicated product, the gist of which is: - The customer buys dollars from the bank over time, at prices that depend on the market price.

- Most of the time, the customer buys dollars at better-than-market rates.

- Some of the time, the customer buys dollars at much, much worse-than-market rates.

Because the product is good for the customer in most scenarios, it has to be really bad for the customer in the other scenarios, to make it an attractive product for the bank to sell. It was an attractive product for the bank to sell. But then the bad scenario came true (roughly, the dollar fell a lot after President Donald Trump's tariff announcements earlier this year), the clients lost a lot of money, and, as clients will, they asked for their money back. "Among those asking for compensation from UBS for the losses incurred are wealthier retail customers who argue they were sold complex products that they did not understand," that sort of thing. And now the Financial Times reports: UBS has ordered bankers to scale back sales of complex currency derivatives after clients suffered heavy losses linked to Donald Trump's "liberation day" tariff announcements. The Swiss bank told advisers to stop pitching the structured FX products — known as Range Target Profit Forwards (RTPFs) — to many clients, according to three people familiar with the discussions, amid growing concerns about sales practices and whether the products were suitable. UBS has already made more than 100 "goodwill" payments to customers who lost money when the US dollar moved sharply in the wake of Trump's April tariff announcements. The bank was now running internal role-play sessions to improve how advisers assess client risk profiles and suitability, one of the people said. "The tone at internal meetings has completely changed in the past few months," the person added. "Now it's all about risk assessment, not boasting about how many clients you got to sign up to these things, which have lucrative fees." One UBS client … said his adviser who had marketed the products had become far more cautious. "This time, my adviser didn't bring any paperwork — just wanted to talk. He said they've been told to stop pushing these." Yes, right, if you have a foreign-exchange derivative product that carries "lucrative fees," that means that the customers don't understand it. (If they understood it, they'd demand lower fees.) If you have a product like that, you will naturally be tempted to sell it to as many customers as possible. And then every so often, something will go wrong, and you'll have to spend a year or two resisting that temptation and having contrite no-materials meetings with the customers to make them feel better. I feel like a cool job would be playing "Naïve Customer" in the internal role-playing sessions that banks use to teach their bankers not to sell derivatives to people who are too unsophisticated. Just the right amount of unsophisticated. We talked a couple of times recently about a weird problem in corporate acquisitions and shareholder activism. The problem is: - You buy a majority of the voting stock of a public company.

- You call up the board of directors of the company and say "hi, I'm the new owner, I have some ideas to spruce up the place."

- The board says "nope, we're happy the way things are, buzz off."

- You say "well but I own the company? I can just replace you and elect a new board that will do what I want?"

- They hang up on you and immediately run out and issue a lot more stock.

- Now you don't have a majority of the voting stock anymore, never mind.

The company is run by its board, not its shareholders, so until you actually remove the board and install your own directors, the directors have a lot of power. There will be a brief delay [1] between when you acquire a majority of the company and when you remove the directors, and during that delay the old directors might be able to take away your majority. Sometimes — as at LQR House Inc., which we discussed recently — the board can do this with an-the-market offering, selling stock to the public to dilute an attempted acquirer. But there is a more classic, more drastic approach: the poison pill. A poison pill (also called a "shareholder rights plan") is a piece of 1980s-era antitakeover technology that essentially provides that, if some shareholder acquires too many shares without the board's approval, all of the other shareholders get a bunch of new shares for free. (We discussed this in more detail when Twitter Inc. briefly adopted a poison pill to protect it against Elon Musk.) This almost never actually happens: Ordinarily, either the potential acquirer goes away without triggering the pill, or the board waives the pill and allows the acquirer to buy the shares it wants. Actually triggering the pill is an administrative and legal mess, so it is mainly used as a deterrent and a negotiating device, not an actual way to issue shares. But not never! Sinovac Biotech Ltd. is a biotechnology company headquartered in China, incorporated in Antigua and Barbuda, and listed on the Nasdaq in the US. In February 2018, it held an annual shareholder meeting, in Beijing, to elect directors. That is usually a boring formality, but that 2018 meeting had some drama: A group of dissident shareholders, including 1Globe Capital LLC and OrbiMed Advisors LLC, showed up and nominated a new set of directors to replace the board. The 1Globe/OrbiMed group got 55% of the votes cast (and about 45% of the shares outstanding), so they thought that they had elected a new board. The old board said, in essence, "not so fast, we need advance notice of director nominations, so this vote was invalid and we are still the board." And then everyone sued. In December 2018, an Antiguan court ruled in favor of the old board, finding that there wasn't sufficient notice of the 1Globe/OrbiMed nominees, so the old board was still the board. (The US Securities and Exchange Commission also fined 1Globe for some disclosure failings, agreeing with Sinovac that it unfairly hid its ownership from the company.) This was a victory for the old board, but perhaps just a temporary one: 1Globe and OrbiMed still owned a lot of shares, and if they filled out the forms right they might be able to force out the old board at the next annual meeting. So the old board tried to issue new shares to dilute them. It did a PIPE (private investment in public equity), selling 11.8 million shares to friendly investors including Vivo Capital. And it took a more drastic step: It declared that the 1Globe/OrbiMed shareholders had triggered Sinovac's poison pill, so each shareholder that did not vote for their nominees would get extra shares, diluting down 1Globe and anyone else who voted for its nominees. Everyone sued about that too. Meanwhile, 1Globe appealed the Antiguan court judgment finding that the old board was still in charge of the company, and that appeal — ultimately to the UK Privy Council — dragged on for a long time. This meant that Sinovac was in several different kinds of limbo [2] : - Nobody was quite sure who was in charge of the company: the old board, or the board that 1Globe might have elected in February 2018.

- Nobody was quite sure how many shares there were, or who owned them: The old board had issued a bunch of new shares to dilute 1Globe and OrbiMed, but it did that after losing the vote at the 2018 annual meeting. If it was not actually the board of the company at that point, then it had no power to issue those shares, so those shares did not exist.

- That creates a problem for Nasdaq, the stock exchange where Sinovac is listed: How could Sinovac's stock trade, if nobody knows which shares are valid? So Nasdaq halted trading in the stock in February 2019; it last traded at $6.47 per share, for a market capitalization of about $380 million. It hasn't traded since.

This is all the sort of silly stuff that happens sometimes at small weird companies. But Sinovac … I mean, it had "vac" in the name. In 2019. You know what happened next? What happened next is that Covid-19 hit, Sinovac developed a vaccine, the vaccine (CoronaVac) was widely used in China, and the company made a bajillion dollars. Its net income grew from about $65 million in 2019, to $185 million in 2020, to $14.5 billion in 2021. I'm not sure that is a particularly ongoing business — SinoVac's revenue fell from $19.4 billion in 2021 to $448 million in 2023, and it lost money that year — but it did generate a mountain of cash for the company. At the end of June 2024, the last time it published financial statements, Sinovac had more than $10.5 billion in cash and short-term investments, more than 25 times its market capitalization when it last traded. This made it rather more urgent to know who owned the stock and who controlled the company. This is fun nonsense for a $380 million market cap speculative biotech company, but for a company sitting on billions of dollars of vaccine revenue, it is quite pressing nonsense. The shareholders whose stock hasn't traded since 2019 might be curious about when they will see some of that money. We talked about this a couple of times, in 2019 when the pill was triggered, and in 2020, when it was working on CoronaVac, and I wrote: What if their vaccine works? What if they are first to market and commercialize it and make billions of dollars? A year ago Sinovac vanished from the public markets as a small-cap speculative biotech company with a weird corporate governance fight, but during its time in the wilderness it might turn into a giant hot biotech company with a Covid vaccine. And a weird governance fight! If the fight over Sinovac was so bitter before, imagine what it will be like when there's real money involved.

Yes. Well. Five years later, in January 2025, the UK Privy Council ruled in favor of 1Globe, finding that 1Globe and OrbiMed were allowed to vote for whomever they wanted at the 2018 annual meeting, even without giving the company advance notice. [3] And so: The New Directors were duly elected at the AGM [annual general meeting] and ... the Incumbent Directors ceased to hold office as directors at the AGM. … The New Directors were therefore validly appointed and the Incumbent Directors have been imposters ever since.

One thing this means is that the poison pill was invalid, OrbiMed and 1Globe are still big shareholders, and their directors were elected. Another thing it means is that the people who ran the company for the last five years — when it was developing CoronaVac and making billions of dollars! — were "imposters" the whole time. After the ruling, the old board put out a press release saying they were leaving nicely, and the new board took over in February and put out its own press release. In April, it announced its plans for what to do with all that CoronaVac money: It was going to declare a cash dividend of $55 per share — roughly $4 billion total [4] — to its shareholders. The stock last traded at $6.47 per share, in 2019, and its all-time high was $10.46 in 2009, so $55 in cash is pretty good. But there's a problem. The old board were "imposters," but they were also "in de facto control of the Company" for almost seven years, and during that time they "purported to issue shares in the capital of the Company to certain persons," meaning mostly the 11.8 million PIPE shares that they sold to Vivo and other friendly investors in 2018. The Vivo group paid real money for those shares, and unlike the poison pill shares it's not obvious that they're invalid. (The new board was "assessing" their validity.) So … can they vote? Control of the company's stock seems to be balanced pretty finely between (1) the 1Globe/OrbiMed group (represented by the new board) and (2) another group, represented by the "imposter" board, backed by Vivo and SAIF Capital. If Vivo's PIPE shares are valid, then the SAIF/Vivo group might have a majority of the stock on its side; if not, then the 1Globe/OrbiMed might have a majority. And so the two groups traded insults and jockeyed for control. In April, the 1Globe/OrbiMed board issued a press release "to Set the Record Straight on the Hostile Actions and False Claims by Vivo Capital." In June, the SAIF/Vivo group won a round in court, when a US federal court found that 1Globe/OrbiMed's disclosures weren't good enough and ordered them to disclose more. Vivo said: This decision affirms Vivo's efforts to restore transparent corporate governance at Sinovac. Given the precedent set by 1Globe, Vivo believes they, along with OrbiMed, will continue their attempts to harm and disenfranchise shareholders until and unless the Board is reconstituted. Vivo has remained steadfast in its mission to restore trust in the Company's governance, and ultimately, in the Company's ability to resume trading and return cash to shareholders, despite 1Globe's attempts to illegally exclude Vivo from exercising our lawful right to vote at the upcoming Special Meeting. ...

And in May, the SAIF/Vivo group called a special shareholder meeting for July, to vote out the 1Globe/OrbiMed board and put in its board. Here's how the 1Globe/OrbiMed board described the plan: SAIF has called this Special Meeting to reconstitute a remnant of the Former Board that the UK Privy Council deemed to be "Imposters" in its final, non-appealable January 2025 ruling. Proposing this slate (the "Reconstituted Imposter Former Board Slate") is the latest scheme by Advantech/Prime Success ("Advantech/Prime"), Vivo Capital (together, the "Dissenting Investor Group"), and other members of the Former Management Buyout Consortium to seize control of SINOVAC at the expense of common shareholders.

Here's how SAIF described it: The Board has not effectively guided Sinovac after the significant chaos of the past several years, including, among other issues, strategic missteps, costly and distracting legal battles, a stock that does not trade, and a large amount of cash that the Company is inexplicably retaining rather than distributing it to shareholders as they should. If elected, SAIF Partners' nominees will work with management to develop a plan to address these issues and bring disciplined corporate governance, proper capital allocation, strategic foresight and operational excellence to Sinovac. The 1Globe/OrbiMed group went to court in Antigua to block Vivo and others from voting their shares, but that didn't work. And so, on July 8, Sinovac held the shareholder meeting, and it was pretty much a rerun of the 2018 meeting, but in reverse. The SAIF/Vivo group showed up, they had more votes, but the current board tried to stop them from voting, and nobody knows if it worked. Here's how the 1Globe/OrbiMed group characterizes what happened: At the July 8, 2025 Special Meeting, SINOVAC Chairman Chiang Li validly adjourned the meeting, to preserve the integrity of the Special Meeting and protect shareholder interests, pending the resolution of litigation in Antigua related to the validity of the 11.8 million shares purportedly issued following an invalid private investment in public equity ("PIPE") to Advantech/Prime and Vivo Capital (together known as the "Dissenting Investor Group").

That is: The meeting happened, but the board chairman (Chiang Li of 1Globe) adjourned it, so nobody actually voted on who should be directors. Here's how the SAIF/Vivo group characterizes what happened: New Directors were elected to the Board at the Special Meeting of the Company held on July 8, 2025, at 8:00 p.m. Atlantic Standard Time. At the Special Meeting, 33,248,861 votes (or 54.71% of the total votes present and voting at the Special Meeting) were voted in favor of the election of the new Directors.

That is: The meeting happened, the shareholders voted, the SAIF/Vivo group won, so its directors are now the directors. So now, after a few months of having one board of directors, Sinovac is back to having two competing boards of directors. We talk from time to time about situations like this, where there is a dispute about who controls a company. The Sinovac situation is unusual in that [5] : - The two groups have switched sides. In 2018, 1Globe/OrbiMed snuck up on the old board and voted for a new board, but the old board said "no that doesn't count" and stuck around. In 2025, SAIF/Vivo snuck up on the new board and voted for a third board (or, I guess, to "reconstitute a remnant" of the old board), but the second board said "no that doesn't count" and stuck around.

- Whoever controls this company also controls just a mountain of cash. I am sure that both sides have views about the proper strategic direction for the company, etc., but at some level the basic situation here is "this company has $10 billion left over from its historical business of selling vaccines in the pandemic, so how do we get it out?"

Has Berkshire Hathaway Inc. ever had an activist shareholder? Besides Warren Buffett I mean. [6] Since Berkshire became the Warren Buffett & Charlie Munger show in the 1960s, it has been a daunting target for activists. For one thing, Buffett owns about 30% of the voting stock. But also he is … Warren Buffett? Like, what, an activist hedge fund manager is going to show up and say "I own 4% of the stock and I think I have better ideas about how to run this business than current management does"? When current management is Warren Buffett? Who is going to listen to that pitch? Who is going to make that pitch? That said, it is no longer exactly the Buffett & Munger show. Munger died in 2023, and Buffett will retire at the end of this year. If the new management underwhelms, maybe in a few years some activist will start getting ideas. But I think a certain halo will persist for a while. "I think this company is mismanaged and undervalued, and we should do some financial engineering to unlock value" is just a tough pitch when the company is Berkshire Hathaway. Daily Journal Corp. is not quite Berkshire Hathaway; it's a small-cap ($560 million) company that publishes newspapers and "supplies case management software systems and related products" to courts and legal agencies. But Munger was a major shareholder and director until his death, and was chairman of the board from 1977 until 2022. It is within the Buffet-and-Munger-show umbrella. But it, uh, has not created quite as much wealth for shareholders as Berkshire has. So this month, an activist shareholder called Buxton Helmsley USA, Inc. started sending letters to Daily Journal (1) complaining about Daily Journal's accounting and (2) offering to fix it. Daily Journal expenses its software development costs, while Buxton Helmsley thinks it should capitalize those costs. If it capitalized them, it would report higher earnings, which might make the stock go up. Buxton Helmsley offered to fix the problem: BH is prepared to lead a disciplined remediation effort aimed at increasing DJCO's market capitalization from approximately $540 million to $700 million through the restoration of GAAP compliance, improved financial transparency, and strategic initiatives.

For its troubles, it asked for 15% of any increase in Daily Journal's stock price. The company said no. Buxton Helmsley sent more, increasingly hostile, letters and emails. Today Daily Journal filed a Form 8-K disclosing all of them and, man, Charlie Munger would be proud. A sample: Two weeks ago, we received a letter from Alexander E. Parker at a firm called Buxton Helmsley USA, Inc. The letter said Daily Journal Corporation (the "Company") should be capitalizing software development costs instead of expensing them under GAAP, and that doing so would "unlock $160+ million in incremental equity value" for shareholders. Mr. Parker then asked for a consulting engagement that would pay him $24 million worth of Company equity if the stock price increased by that amount for any reason (i.e., $.15 of every dollar), and he asked for two seats on the Company's Board of Directors. ...

Mr. Parker seems to fancy himself a whistleblower, but the Company has been disclosing its practice of expensing software development costs and the reasons for that in its public filings for more than a decade. … Furthermore, the Company's approach has been reviewed as part of the annual audit without issue by three different national accounting firms since those development efforts began.

Mr. Parker is right that if the Company capitalized those costs, it would boost near-term earnings and asset values by reducing the Company's expenses and shifting them to the balance sheet. Anyone who knew our longtime Chairman, Charles T. Munger, knows what his thoughts would have been on the idea of "creating value" through accounting.

Daily Journal engaged an independent consultant to review its accounting, but "that's when Mr. Parker's game became clear": On July 23, one day after being informed of the decision to engage an independent accounting firm rather than Buxton Helmsley, Mr. Parker fired back a letter saying that only Buxton Helmsley was qualified to "restore trust" while at the same time notifying us that he was reporting the Company to the Enforcement Division of the SEC. That letter is attached as Exhibit 99.3. You should read it.

We suspect Mr. Parker will learn with age and experience that few people want to work with someone who presents himself this way. Even fewer want to work with someone who reports them to the government when he doesn't get what he wants! Also, we've already reached out to the SEC staff and have offered to discuss with them the Company's software development accounting and/or Mr. Parker, should they so desire.

I tell you what, if you are a public company looking to brush off an activist investor, and that activist is not Carl Icahn, it's hard to do better than saying "We suspect [activist] will learn with age and experience that few people want to work with someone who presents himself this way." Though it does help if you can add, as most companies can't, that "anyone who knew our longtime Chairman, Charles T. Munger, knows what his thoughts would have been" about whatever financial engineering the activist wants to get up to. I wrote yesterday about why you might buy home insurance from an insurance company that doesn't have much money and might not be able to pay your claim. I suggested two answers: - You have not done extensive due diligence and don't realize that the company doesn't have much money; or

- You don't really want insurance, you're happy to take the risk, but somebody else (e.g., your mortgage lender) demanded that you get insurance, so you get the cheapest and worst insurance you can get.

A couple of readers emailed with a third, possibly more important answer. That answer is: You want insurance against uncorrelated risks, but are not worried about correlated risks. That is: If you live in a hurricane zone, and you buy home insurance from a thinly capitalized insurance company, and then your house burns down in a freak accident, the insurance company will probably pay your claim, no problem. The company doesn't have that much money, but it has enough money to pay for your house. You want insurance against freak accidents, and that's what you're getting. But if there's a hurricane, and your entire neighborhood is flattened, that's when your insurance company might be in trouble. It has enough money to pay a few claims for freak accidents, but not enough to pay everyone's claims at once. If there are a lot of claims at once, nobody gets paid, which means you don't get paid. Whatever your insurance policy says, what it actually does is insure you against freak accidents that affect you, not widespread disasters that affect everyone. Why would you want this sort of insurance against only uncorrelated risks? Perhaps you have idiosyncratic views about the probabilities of particular risks. (You think hurricanes are fake, but you smoke in bed?) But the more likely answer involves bailouts. "Surely," you think, "if my whole neighborhood is flattened and our insurance company goes broke, the government will do something about it." Is that true? I don't know, and this is not financial advice. But as a general model it makes a kind of sense. I once wrote about taxi insurance, of all things, that the model here is: Write insurance on some essential part of the economy. Underprice the insurance: Charge $60 for insurance that will predictably pay out $100 in a few years. Win a lot of market share: Your insurance is cheaper than everyone else's, so customers will prefer you. Invest the float and pay yourself nice bonuses. Eventually, you will get insurance claims, you won't have enough money to pay them, and you'll be insolvent. Oops! It's fine, though. The thing you are insuring is so essential that the government will probably bail you out.

Certainly it fits a broad pattern in the financial industry, where people talk a lot about wanting uncorrelated risks, but where social pressures and structural features cut the other way. It is acceptable to lose money when everyone else does, but embarrassing to lose money all by yourself. And when you lose money by yourself, that's your problem; when everyone loses money at once, that's a societal problem, and the government might do something about it. Union Pacific to Buy Norfolk Southern in $85 Billion Deal. AI Is Wrecking an Already Fragile Job Market for College Graduates. Robinhood CEO Says It's a ' Tragedy' Retail Can't Tap Private Markets. Oil Giant Vitol Hands Record $10.6 Billion Payout to Its Traders. Tesla, Samsung Sign $16.5 Billion Deal to Make AI Chips. Baseball's 'Spot-Fixing' Investigation Now Includes a Star Closer. Harley Davidson Nears Financing Unit Deal With Pimco, KKR. Can Botswana take control of diamond giant De Beers? Almost Every Corner of Emerging Markets Is Surging as Dollar Sinks. Top Justice Department Antitrust Officials Fired Amid Internal Feud. ECB staff accuse Christine Lagarde of running 'unaccountable legal fortress.' Denver Pastor and Wife Face Charges in 'God-Inspired' Cryptocurrency Scheme. (Earlier.) The Short-Lived Plan to Produce a Trump-Themed Instant Pot. The Criminal Enterprise Run by Monkeys. If you'd like to get Money Stuff in handy email form, right in your inbox, please subscribe at this link. Or you can subscribe to Money Stuff and other great Bloomberg newsletters here. Thanks! |

No comments