| It's not just US exceptionalism that has taken a beating this year. The same can be said for Japan's status as the exception to all economic rules. The voters have just rubbed that home by depriving the long-ruling Liberal Democratic Party of a majority in the upper house in the weekend's election. It had already lost its hold over the lower house, leaving Japan's traditional hegemonic party without control of either chamber of the legislature for the first time since 1955. Shigeru Ishiba, who took over as prime minister last year, says he intends to continue, and must now put together a new coalition. At the time of writing, with the breakdown of seats still unclear, prediction markets think his chances of survival, still bad, have improved marginally: The yen has strengthened a bit, showing that markets largely expected this. Bond and equity markets are closed until Tuesday, when a more serious reaction will begin. Equity futures aren't much impacted so far. Longer term, Japan's shift is undeniable. Jesper Koll, a long-time investment banker in Tokyo who writes the Japan Optimist newsletter, says: Make no mistake — this is about so much more than the tariffs: The ruling LDP's foundational raison d'être was to be America's independent but loyal agent in liberated-by-America-now-democratic Japan; and this core is exactly what is is being disrupted — the emerging realities of America's new national priorities, economic agenda and undemocratic leadership style are, simply put, unacceptable to the Japanese people, thus undermining LDP credibility.

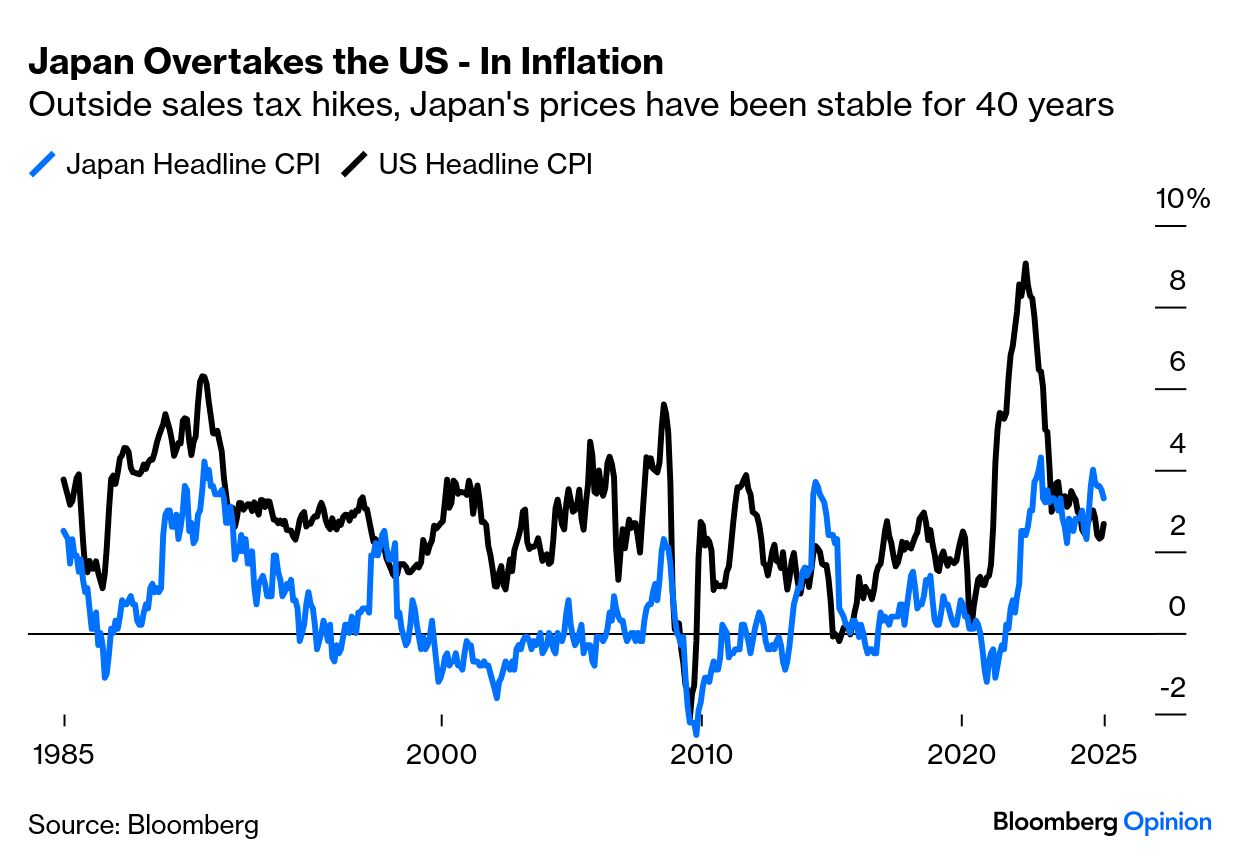

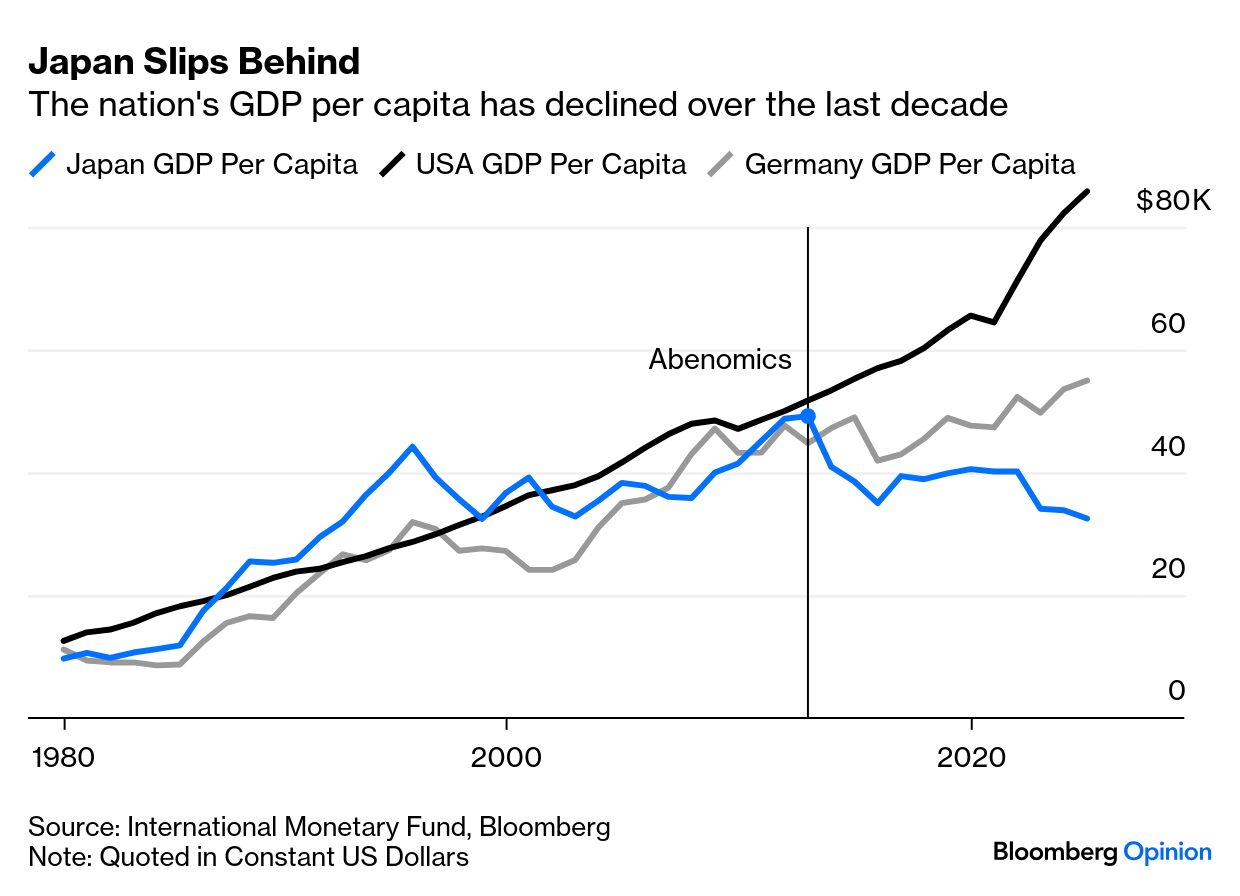

In some ways, the voters are ratifying bond markets' verdict. Thirty-year Japanese Government Bonds yield as much as 3% for the first time in more than two decades. The pandemic seems finally to have broken the country's long Ice Age: That can be seen most clearly in inflation numbers. Outside of a couple of ill-judged sales tax hikes, which automatically drove up inflation for a while, Japan's inflation has barely ever exceeded US CPI in the last four decades. That's where it is now: It shouldn't be surprising that Japan's electors are acting like those in most every other country in the developed world, and punishing the politicians who allowed this to happen. That's one critical way in which Japan is no longer so exceptional. Another is in economic growth. Japan's population is falling, so overall gross domestic product can be misleading. Judged by GDP per capita, Japan was ahead of the US and Germany well into the 1990s, and kept pace until after the Global Financial Crisis of 2008. Starting with the "Abenomics" policy adopted in 2012 by the late Shinzo Abe to shake Japan back into life, that changed. It weakened the yen, and in dollar terms GDP per capita sharply parted company with the other two big developed economies: This election is not as dramatic as others of the post-pandemic era, and no full-throated populist alternative is on offer as yet. But it looks like we should assume that Japan has completed normalizing, and not in a good way. It's no longer immune to inflation, and the populace doesn't like that. |

No comments