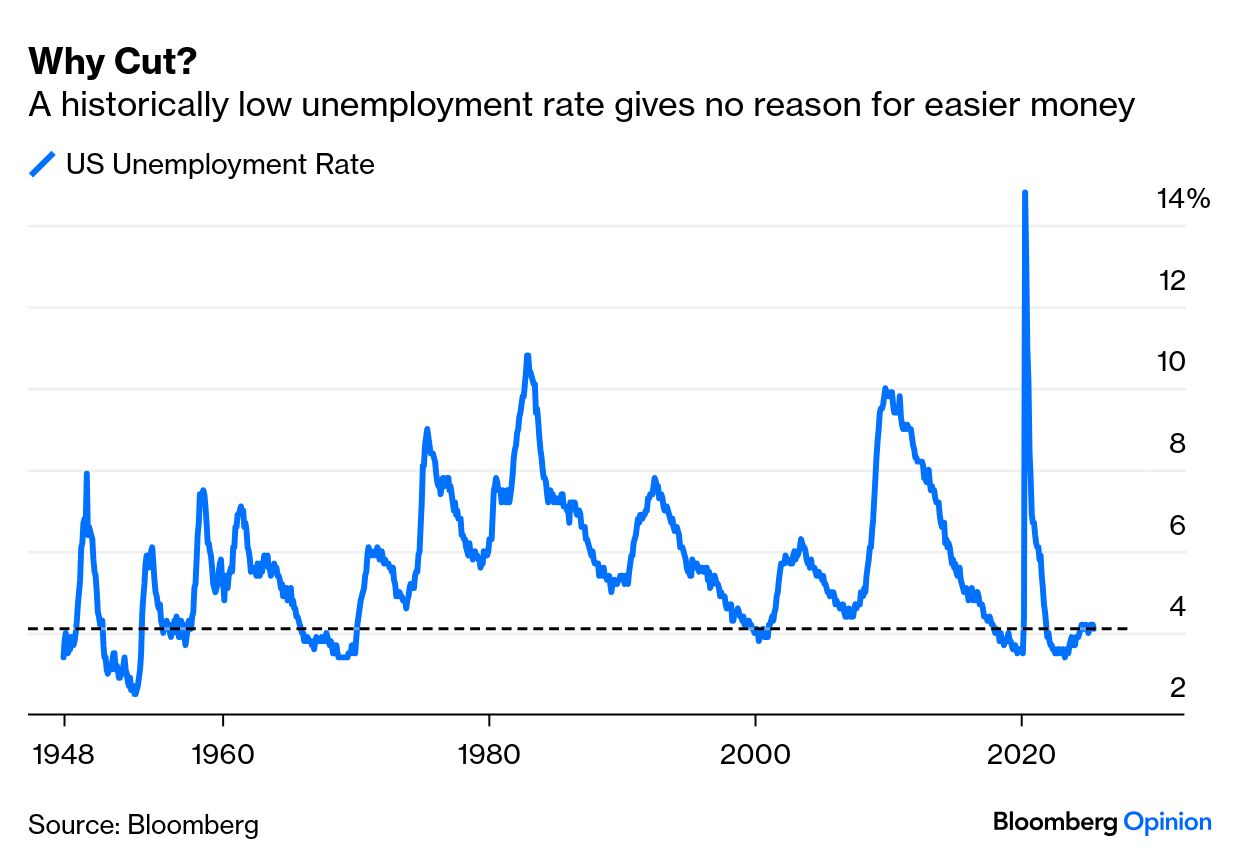

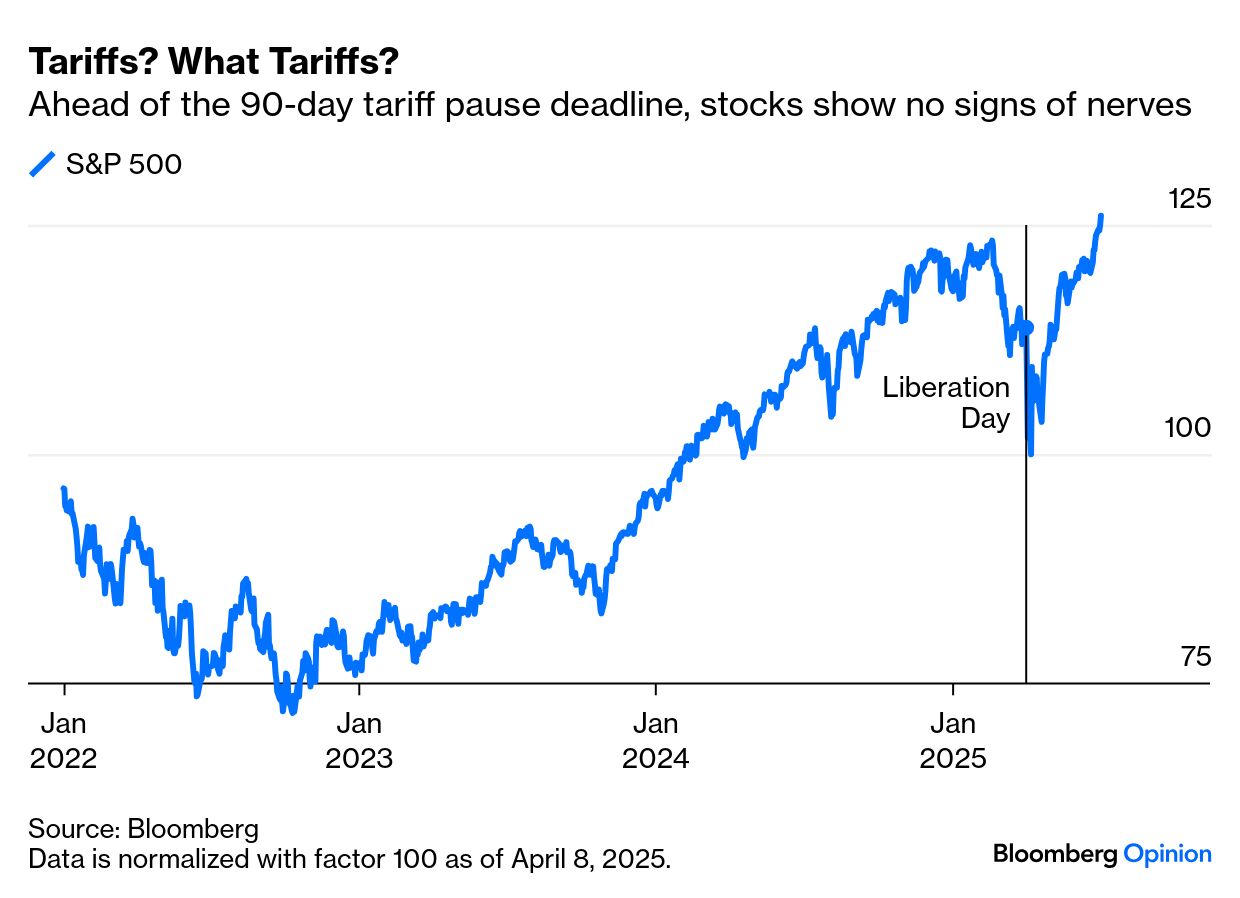

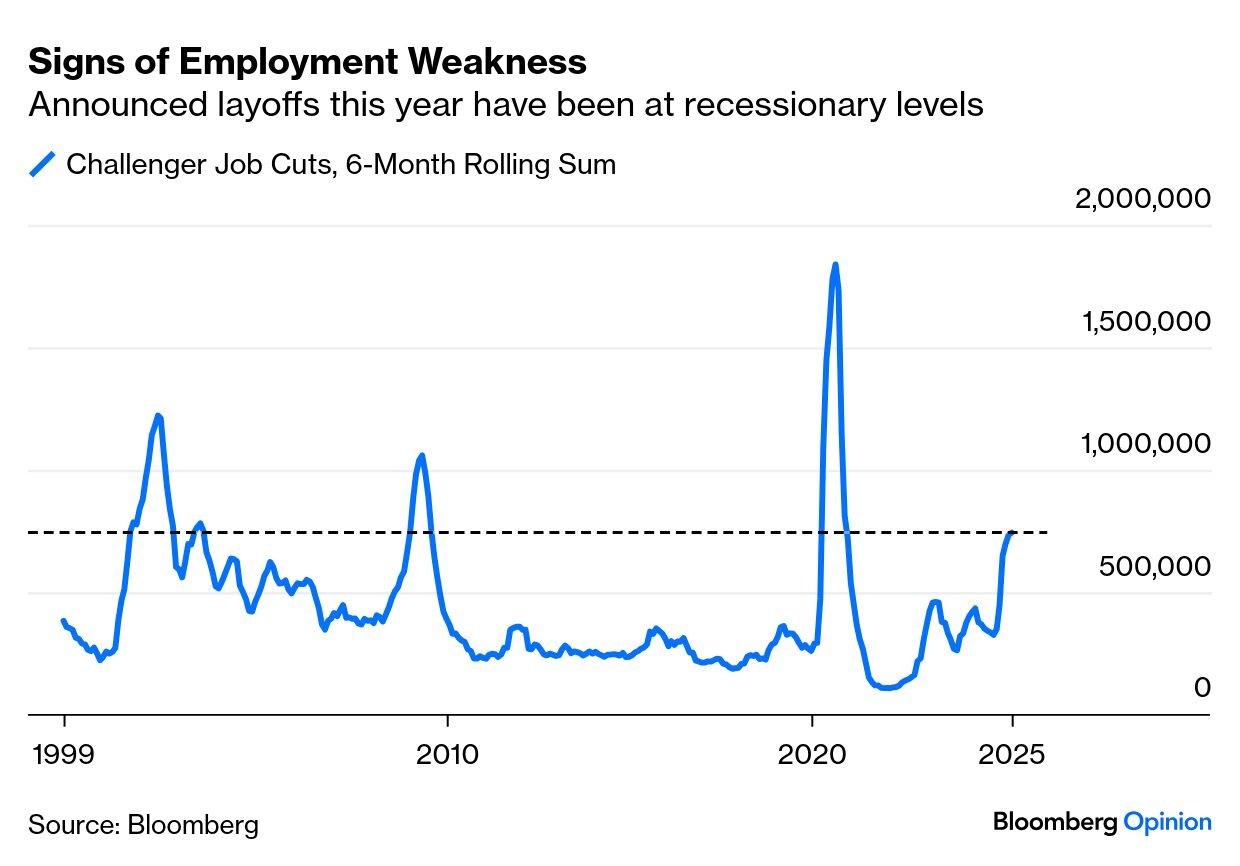

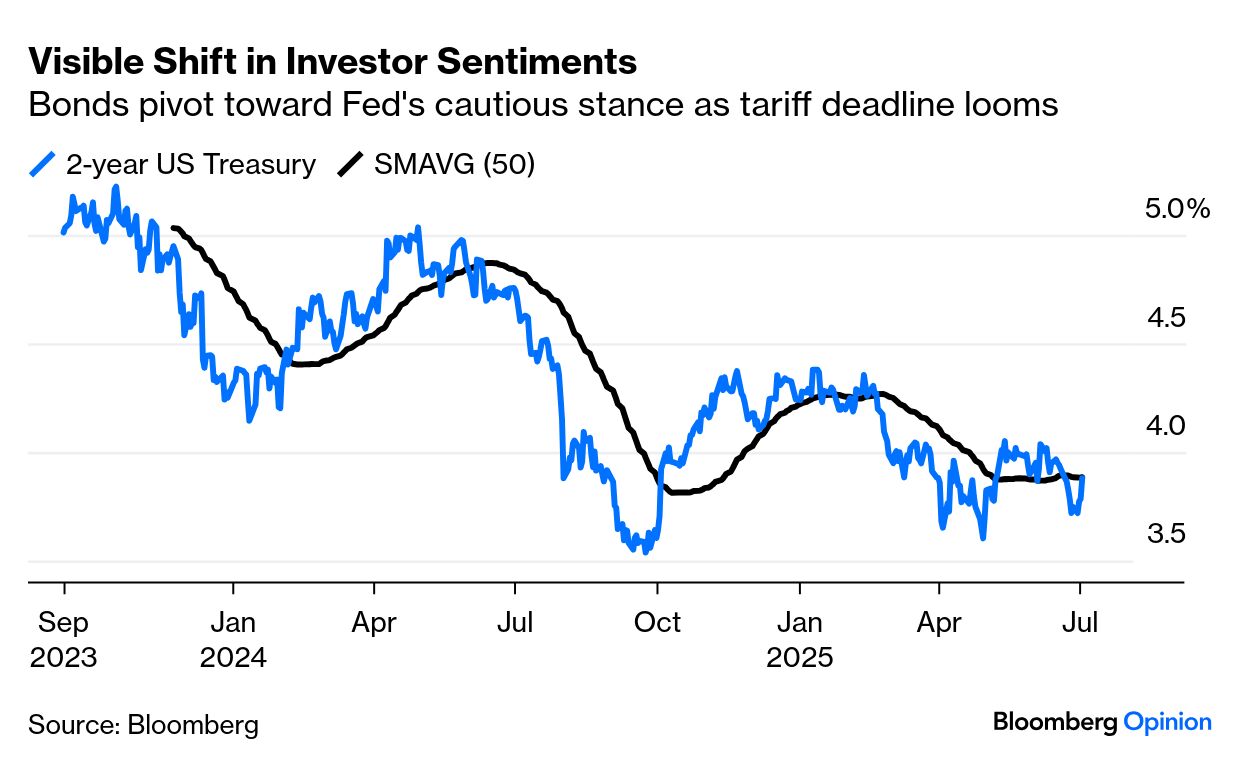

| For a brief moment ahead of Thursday's job data, economists thought a deterioration would guarantee a rate cut in September, or even prod the Federal Reserve to move this month. Not so fast. Instead, stronger-than-expected numbers slashed the odds for a September cut, and extinguished hopes of an ease in July. The unemployment rate fell to 4.1% — a historically low level that suggests on the face of it that current rates are doing no harm whatsoever: At this point, the Fed's cautious approach is paying off, amid much impatience from the president and others. Within the rate-setting Federal Open Market Committee, the differences are only over timing, with 10 policymakers foreseeing at least two cuts this year, and seven projecting no cuts. Another two penciled in just one. That isn't so far different from the market. Bloomberg's World Interest Rate Probabilities function, which derives implicit policy rates from futures prices, shows two cuts by year's end. This is less than in the immediate aftermath of the Liberation Day tariff announcement in April, but the futures market thinks that will be counterbalanced by more cuts next year. Their estimate of rates by the end of 2026 has barely changed since April: For stocks, good news on the jobs market more than counteracted the bad news of a dwindling chance of rate cuts. The S&P 500 set a new record. Remarkably, it has regained 26% since its nadir on the eve of the 90-day tariff moratorium three months ago. The approaching end of that pause appears to be causing no worries at all: The employment picture remains confusing. The outright jobs reduction shown by June's ADP National Employment Report for the private sector, immediately followed by a decent beat for non-farm payrolls, was as confounding as reassuring. Liz Ann Sonders of Charles Schwab pointed out that the regular count of announced cuts by Challenger, Gray & Christmas had shown layoffs on a scale only previously seen ahead of recessions, on a rolling six-month basis: On balance, bonds accept that the labor market isn't weakening enough to drive rate cuts. A slump in shorter-term Treasuries, most sensitive to rate expectations, was a reasonable reaction: The bond market clearly wasn't expecting such a strong jobs report, which also included upward revisions for April and May. As Brandywine Global's Kevin O'Neil notes, while easing inflation supports the case for Fed rate cuts, a 4.1% unemployment rate suggests very little need for them. The impact of the DOGE federal job cuts earlier in the year may have distorted perceptions: Notably, the gains came from the government sector, which had seen subdued job growth this year in part due to the administration's initiatives. In terms of bond action, Thursday's data will likely help reverse some of the yield curve steepening that's taken place in recent weeks.

Is the market's view based on solid jobs growth justified? Bloomberg Economics' Anna Wong argues that there's no definitive conclusion that the labor market is in solid shape; the unemployment drop was due to exits from the labor force (meaning fewer people were seeking work — possibly a result of the sharp fall in the number of arriving immigrants), while payroll gains were exaggerated by a Bureau of Labor Statistics model that seeks to measure the impact of business formations and closures: Details indicate that hiring in private service jobs slowed in June as the cancellation of federal government contracts hits the education and health sectors. There's little evidence of an impact on payrolls from the trade war, as the logistics sector held up as firms continue stockpiling inventory. We maintain our view that the FOMC will only cut interest rates once in 2025, at the last meeting of the year in December.

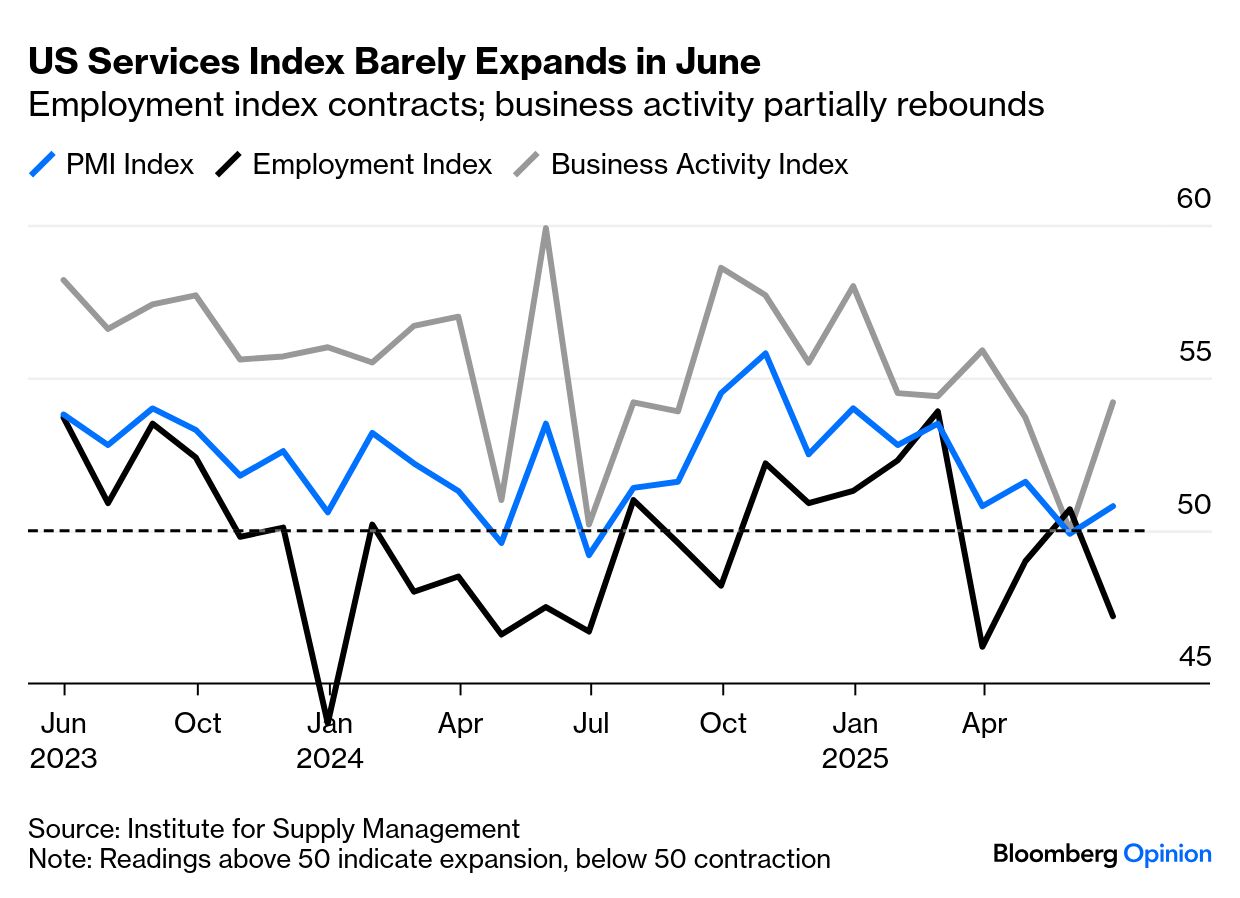

This is a significant shift from earlier sentiments — driven largely by ADP's report — that a 50-basis-points cut in September was emerging as a possibility as the Fed discovered it had fallen too far behind the curve. A pick-up in business activity and bookings allays those fears for the time being, while the latest Institute for Supply Management index for services showed the sector (just) in expansion territory, reversing May's descent into contraction: If a jumbo cut remains a low probability, Standard Chartered Bank's Steven Englander argues that the advantage of discussing a 50-basis-points move is to show a willingness to meet President Donald Trump's demands for lower rates, while giving time for data to justify it: The result may be near-term volatility as markets grapple with the alternatives. Our baseline remains one cut, and we don't think the FOMC will change its projections much, but the discussion of a 50-basis-points cut may lead to markets seeing the outcome as somewhat dovish, even if coolness on a July move could introduce some hawkish moments.

A jumbo cut would require a significant decline in inflation and an outright fall in payrolls. Otherwise, Anwiti Bahuguna of Northern Trust sees little chance for an outsized rate cut over one bad payroll and a slight slowdown in inflation. As Jay Powell noted to Bloomberg's Francine Lacqua, without tariff threats, the Fed would probably have cut already. It's still not clear that the levies to date have had a negative impact on jobs. Inflation numbers this week will shed light on whether they are being passed on to consumers. The long wait for clarity, Cetera Financial Group's Gene Goldman argues, raises the risk of an error. Goldman expects at most a 25-basis-points cut this year and then a faster easing in 2026, with clarity on inflation and the labor market achieved: The next year, because the Fed goes from being preemptive to reactive, they're going to cut rates a lot more. The chance of a policy error increases dramatically because the longer they wait, the more this is an anchor on the economy. But they have to wait because inflation is still too high.

Throw in the pressure from the White House and the FOMC's job gets no easier. Powell, who bows out in less than a year, knows the credibility and independence of the central bank's policies are in doubt. At present, it's still impossible to see how he can accede to the president's wishes and cut. —Richard Abbey |

No comments